Morocco, on the northwest corner of the African continent, might not seem to have a major involvement in the automotive industry. Although the country of 37.3 million people began assembling motor vehicles in 1959 with a state-owned company, its auto industry only began to really develop after the company was privatized in 1990. By the early 2000s, the government decided to develop its auto industry into a manufacturing hub for Europe and provided a suitable environment to attract major carmakers.

According to the government, the country now has 10,000 automotive design engineers for German, British, French and North American brands, and this number is expected to reach 50,000 in the coming 3 years.

August was a good month for the carmakers in Malaysia as improved production output enabled them to deliver more vehicles. Like Proton, market leader Perodua also reported significantly higher numbers for its August deliveries with 26,039 units registered nationwide or 42% more than in July.

“We are currently trying to build on this production improvement to ensure speedier delivery to our customers,” Perodua President & CEO, Dato’ Sri Zainal Abidin Ahmad.

The Bezza had the highest output in August but the Myvi remains the brand’s bestseller.

Bezza output highest Of the 28,036 units produced in August, the Bezza accounted for the most number (24.2%), closely followed by the Myvi which accounted for 22.2%. The Axia output was the third highest with 4,857 units (17.3%) leaving the factory in Sg. Choh, Selangor.

“For the newly launched Alza, we have received bookings of 51,000 units so far,” said Dato’ Sri Zainal, adding that 7,682 units registered in July and August. An average of over 1,000 orders were received daily in the first 27 days after bookings opened, swelling the order bank to over 30,000 orders by launch day.

10 months to get Alza? With production of the new Alza having started in June and a targeted volume of 3,000 units a month, the already large number of orders means that the waiting period could stretch to 10 months.

The cumulative volume of deliveries achieved for the first 8 months of this year shows an increase of 63.7% to 171,728. In the same period in 2021, 104,933 units were registered nationwide.

Dato’ Sri Zainal points out, however, that this comparison must also be seen in the light of the country having a lockdown situation between June 1 to August 15 last year. During that time, all non-essential operations were stopped, including vehicle production and sales activities.

The ‘King’ is still bestseller “The Myvi remains our bestseller this year with 48,658 units delivered, followed by the Bezza with 39,642 units, and the Axia 37,013 units,” he said.

Supply better but costs rising Dato’ Sri Zainal said the improvement in production and sales came about as some key issues have been resolved at the moment. These issues relate to the global semiconductor chip supply shortage and insufficient labour at some suppliers’ operations which lead to disrupted supply of some components.

“We are also closely monitoring the increase in prices of raw materials at the moment and are working with the ecosystem on how best to mitigate this impact to our production operations,” he added.

To know more about Perodua’s products and services, visit www.perodua.com.my.

Although it had a slow start to 2022, Proton’s production has now risen substantially and in August, deliveries totalled 15,880 units (including export sales). It was the best sales month for the Malaysian carmaker since July 2013, 109 months ago.

Cumulatively, for the first 8 months of the year, sales of Proton vehicles reached 87,481 units, a 39.7% over the 62,637 achieved between January and August 2021. By Proton’s estimate (based on the expected Total Industry Volume of 66,900 units), that would give it a market share of 19.5%, with the August numbers alone taking the share to an estimated 23.7%.

The company remains focused on ending 2022 with a fourth consecutive year of volume growth.

Sales leadership Despite the recent launch of new direct rivals from other brands, Proton has maintained its position at the top of the SUV segment. The X50 reached a third consecutive month where deliveries crossed the 4,000-unit level with 4,329 units delivered in August. It’s the first time an SUV has achieved such a feat in Malaysia and comes on the back of its industry record with 4,763 units in July.

Click here to find out how you could win a new X50 by just spending RM30.

The larger X70 contributed 1,555 units in August, bringing Proton’s total SUV sales for the month to 5,884 units. The cumulative volume for 8 months is now at 37,489 units.

On the passenger car side, the Saga also benefited from improved component supply as 6,156 units were delivered last month. Demand for the latest Saga remains high and total deliveries have exceeded 14,000 units since its launch in May this year.

The biggest beneficiaries of the increase in production volume were the Persona and Iriz. 2,612 units of the Persona were delivered nationwide, the highest number since February 2020. For the Iriz, the 962 units delivered were at a sales level not since April 2021.

Stabilised production “With four months to go in 2022, Proton’s production operations have stabilised. Critically, our component supply is now more consistent and better managed to ensure we can produce as many cars as possible. With that in mind, we have undertaken an initiative to increase the number of delivery trucks by over 100% by the end of the year. This makes it easier to ensure our dealers receive their stock as quickly as possible and, in turn, this benefits our customers who have been patiently waiting for their vehicles,” said Roslan Abdullah, Deputy CEO of Proton.

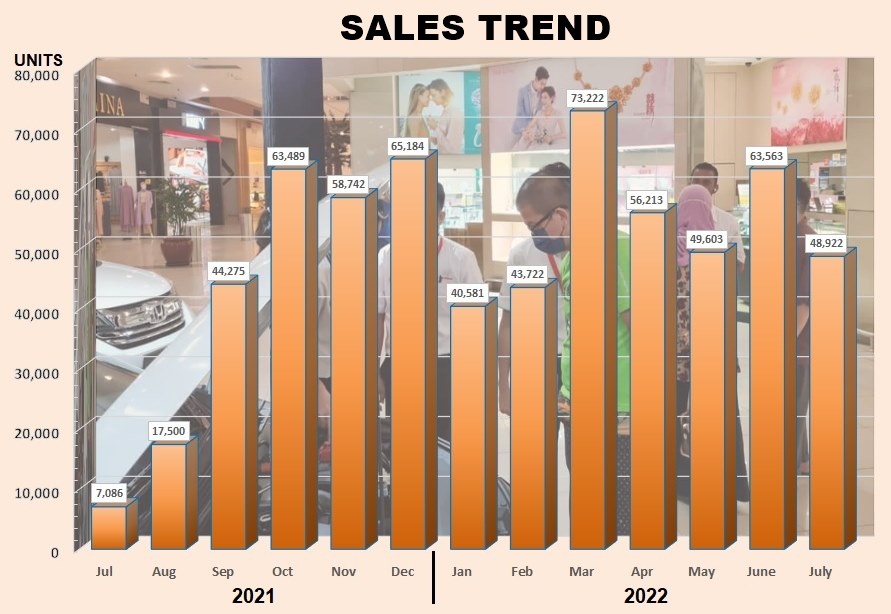

As expected, sales in July 2022 fell and the Total Industry Volume (TIV) dropped 23% to 48,922 units. The reason was partly due to June being exceptionally high as many people rushed to buy their new vehicles before the sales tax exemption ended. Whatever stocks companies had were quickly exhausted during the month and the TIV might have been higher if there had been more supply.

For those who managed to confirm their bookings by the last day of June 2022, the sales tax exemption will still apply for their new vehicle, provided it is registered not later than March 31, 2023. That should be ample time for the assembly plants to supply the vehicles.

Looking back at 2021, the TIV this year is certainly higher. In July last year, due to the MCO and restrictions, sales fell to less than 7,500 units for the month. On a cumulative basis, the TIV has reached 380,595 units after 7 months, 48% higher than the volume for the same period in 2021.

On the production side, from January to July this year, 369,994 vehicles were assembled locally, almost 126,000 units (52%) more than for the same period last year. However, the chip and parts shortages continue to slow down output as vehicles cannot be completed. This affects both locally assembled as well as imported models since the chip shortage is global.

The Malaysian Automotive Association expects August sales to be at the same level as July. The association revised its annual forecast upwards by 30,000 units to 630,000 units. This means that average monthly sales will have to be about 50,000 units in the remaining 5 months.

The situation at the moment is not a true picture of the state of the market as the number of registered vehicles reported to the MAA is largely dependent on whatever stocks are available from the plants or from overseas. Until the supply situation stabilizes, it will be hard to ascertain the demand since every available unit is delivered as soon as it arrives at the showroom.

With the accelerated pace of development in industries, a revolution is taking place and where the automotive industry is concerned, this revolution will take companies to the next level with cutting-edge technologies, processes and machinery. This transformation of the automotive industry is referred to as Industry 4.0., a term inspired by Germany’s ‘Industrie 4.0’, a government initiative to promote connected manufacturing and a digital convergence between industry, businesses and other processes.

To promote the adoption of Industry 4.0, the Malaysian Investment Development Authority (MIDA) and Perodua are gearing up through a strategic partnership to introduce the MIDA-Perodua Digital Transformation Ecosystem Programme. The programme aims to upgrade local automotive suppliers and to digitalise their manufacturing processes through adoption of Industry 4.0.

Developing local players’ capabilities “Local companies play a major role in building the nation’s industry ecosystem–geared to support large companies and MNCs. The initiation of the MIDA-Perodua collaboration in 2020 was crucial to ensure a steady development of our local player’s capabilities in the automotive industry,” said Datuk Arham Abdul Rahman, Chief Executive Officer of MIDA.

“Under MIDA’s initiative to facilitate these companies to adopt digitalisation and Industry 4.0, we have been successful to contributing immense growth in Perodua’s manufacturing volume, through the empowerment of its industry partners and service providers.” he said.

Dato’ Sri Zainal Abidin Ahmad, President & CEO of Perodua.

Local technology ecosystem development According to Dato’ Sri Zainal Abidin Ahmad, Perodua’s President & CEO, the MIDA-Perodua Digital Transformation Ecosystem Programme is aligned with the government’s efforts to enhance local technology ecosystem development activities in terms of supply and value chains, research and development activities, and innovation and commercialisation. The programme has shown a promising sign as the first group of participants had implemented their proposed projects.

“The implementation of Industry 4.0 is not only for the automotive supplier’s benefit, but the impact of this programme will contribute greatly to the national’s digital transformation agenda. The programme also can fast-track Malaysia’s industries, from small to large, as it provides both funds and guidance,” Dato’ Sri Zainal Abidin said.

“Perodua’s role has always been to develop the automotive ecosystem and this programme is another example of our commitment towards this objective,” he added.

Eight participants in programme The first phase of MIDA-Perodua strategic partnership has brought forth three potential Perodua-friendly partner – LSF Technology Sdn.Bhd., J.K. Wire Harness Sdn. Bhd. and Autoliv Hirotako Safety Sdn. Bhd. These companies have also been granted Domestic Investment Strategic Fund as part of the government’s initiative to assist the local companies to embark into the global supply chain.

Moving forward to Industry 4.0, MIDA and Perodua have identified five more vendors with much potential and growth opportunities. These are Armstrong Auto Parts Sdn. Bhd., Ingress Aoi Technologies Sdn. Bhd., Namicoh Suria Sdn. Bhd., P.D. Kawamura Kako Manufacturing Sdn. Bhd. and Kumpulan Jebco (M) Sdn. Bhd.

MIDA, being the pivotal principal promotional agency of Malaysia, will be extending their support services to help more companies obtain growth in terms of productivity, talent and bridging financial and technology gaps.

The agency is confident that through such facilities and empowerment measures, these automotive players will be able to increase their business offerings and expertise to innovate its products and services and climb the supply chain ecosystems.

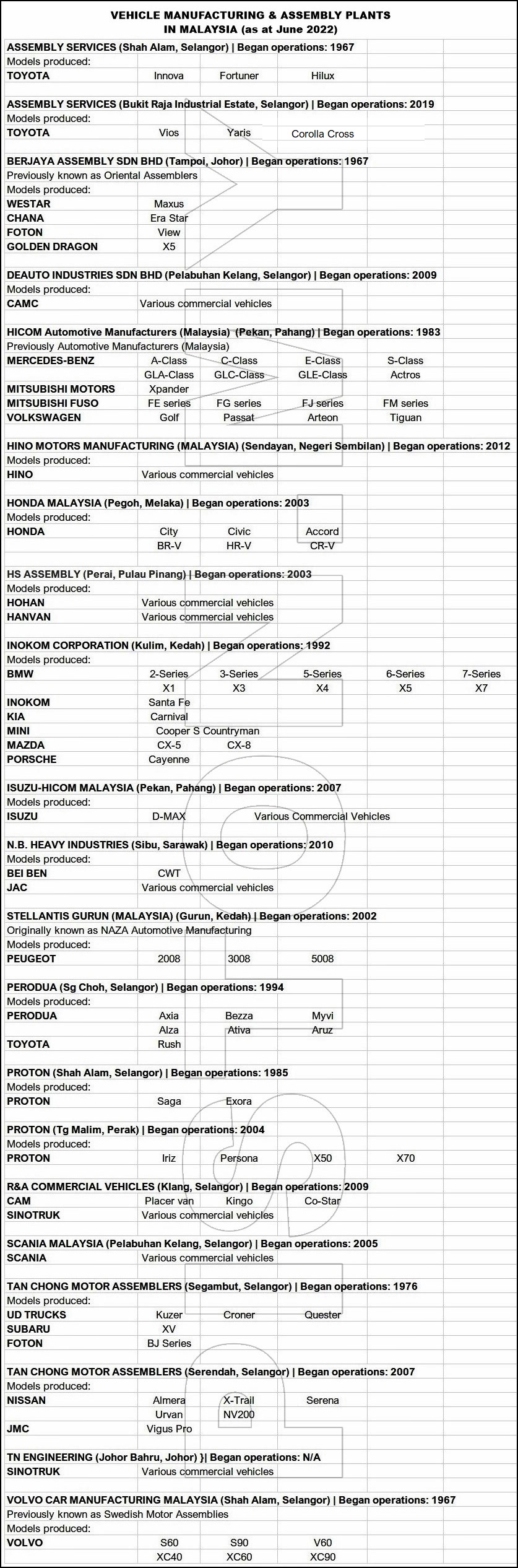

It’s now 55 years since the first new vehicle assembly plant began operations in Malaysia. Volvo, together with its local partner, Federal Auto, were the first to introduce a locally-assembled model in 1967 after the government had announced what could be considered as the first national automotive policy in the mid-1960s.

The policy was intended to attract foreign carmakers to assemble some of their models locally and if they did so, they would be given incentives in the form of lower tax rates. This would enable them to sell at lower, more attractive prices compared to the models that were imported in completely built-up (CBU) form.

Swedish Motor Assemblies in Shah Alam, Selangor, was the first assembly plant to start operations, rolling out the Volvo 144 in 1967 as the first locally-assembled model. The plant is still in operation today assembling the latest Volvo modelsfor the region.

The locally-assembled vehicles were assembled from CKD (completely knocked-down) packs of parts sent from bigger factories in Europe, Japan and North America. To help develop a local automotive industry – an important catalyst for industrialization – the government also listed certain parts for mandatory deletion. Assemblers had to obtain them from local companies, many of which had also been set up in tandem with the new assembly plants.

The parts were items like windscreen glass, paint, tyres, wire harnesses, etc and if the assembler chose to still import them, then there would be a penalty for doing so. Over time, revisions in policies saw an emphasis on getting assemblers to source more parts locally and targets were set for local content.

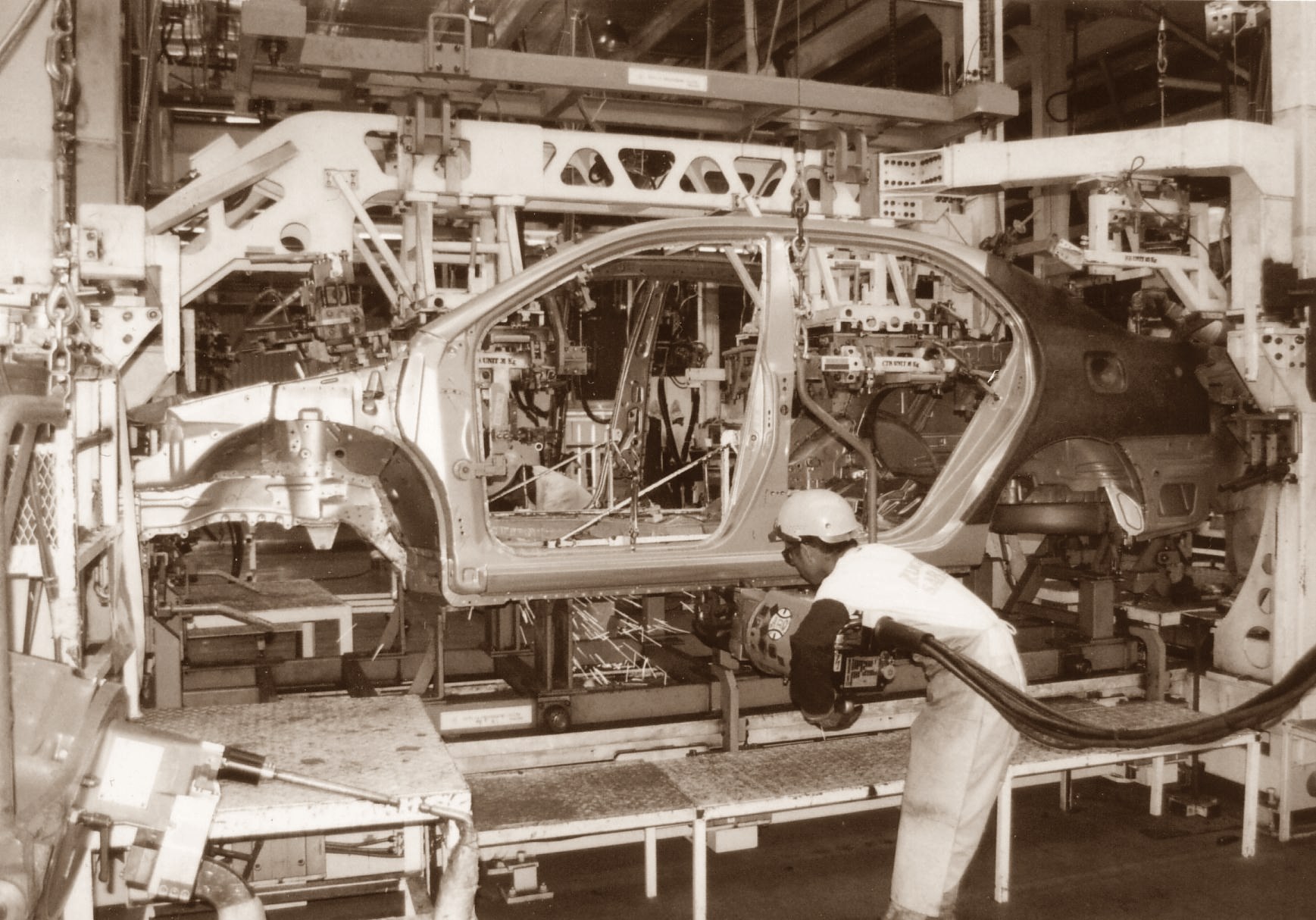

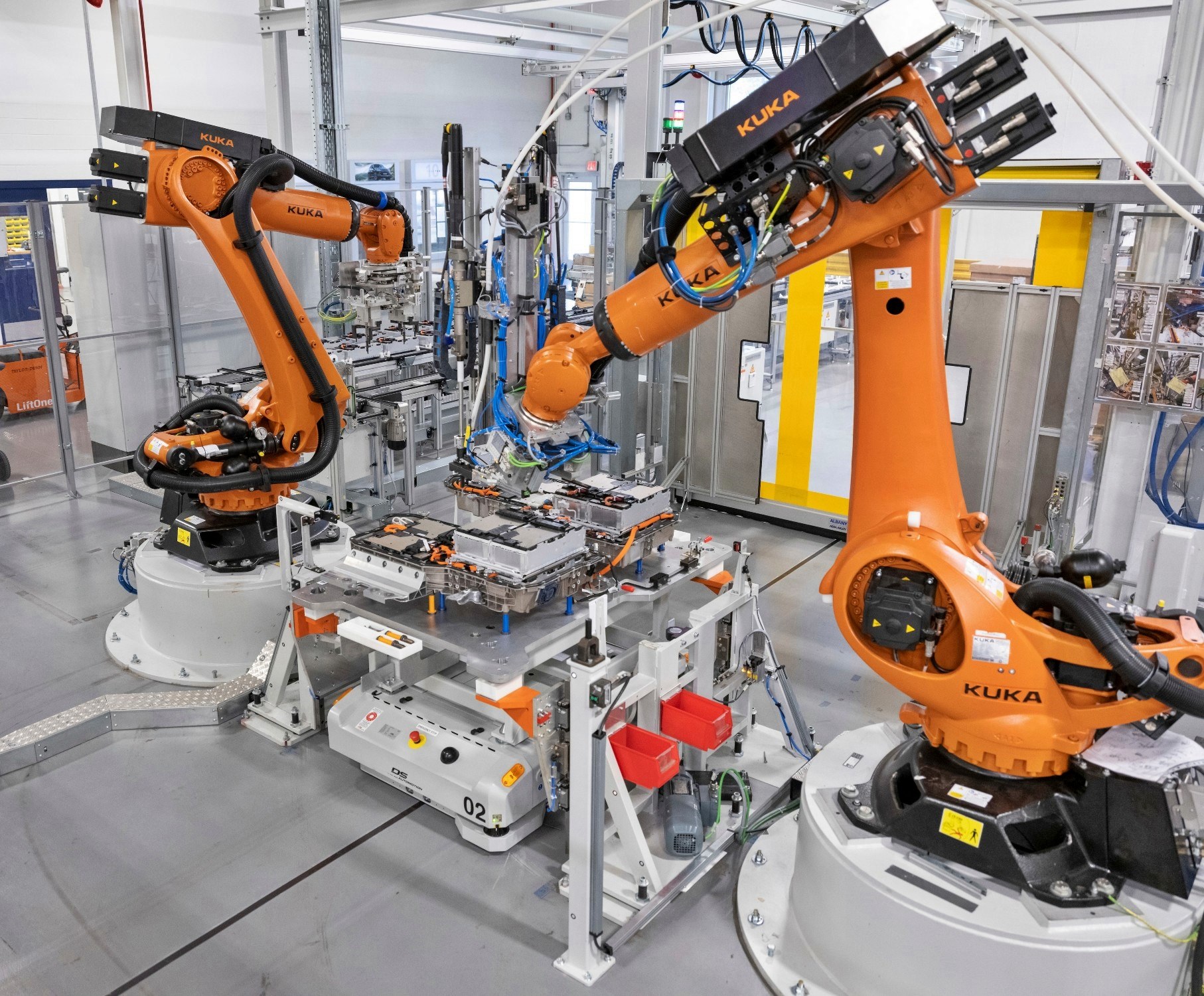

From manual welding of parts by human workers in earlier years (above), many of the plants today have automated welding processes done by robots. Shown below is the X70 body welding line at the Proton factory in Tg. Malim.

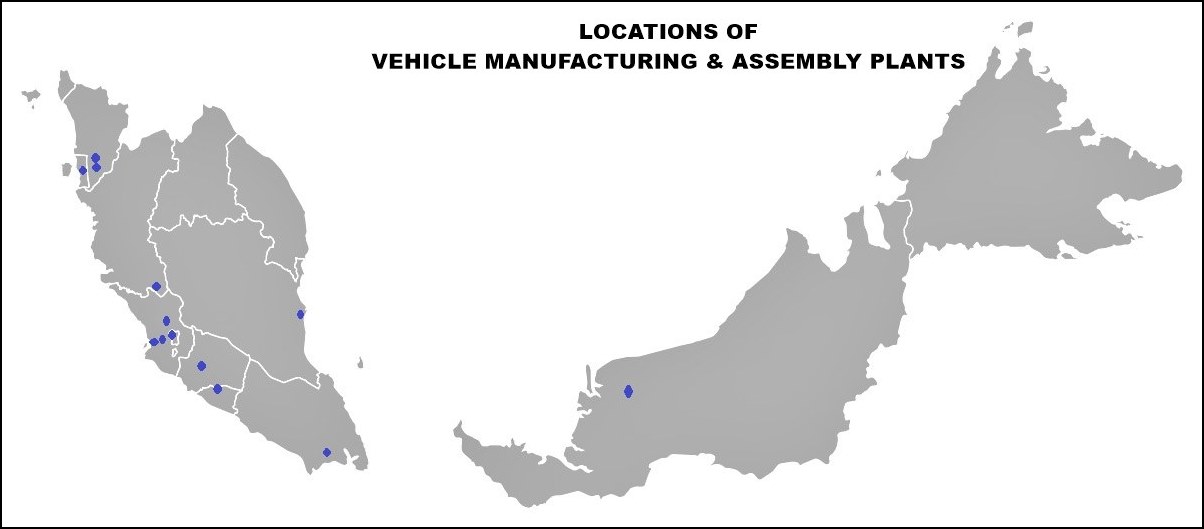

The first batch of assembly plants were opened in two areas – Tampoi in Johor and Shah Alam in Selangor. By the 1980s, other locations were also chosen in Sarawak, Sabah and Pahang. Selangor saw the most activity in the early years and the Klang Valley remains a major automotive hub today. In the 1990s, new plants were opened in Kedah and Proton and Perodua also built plants outside the Klang Valley. Honda and Hino chose sites in Melaka and Negeri Sembilan, respectively.

Source: Malaysian Automotive AssociationPorsche Cayenne assembly at Inokom in Kulim, Kedah.Proton factory in Tg Malim, Perak

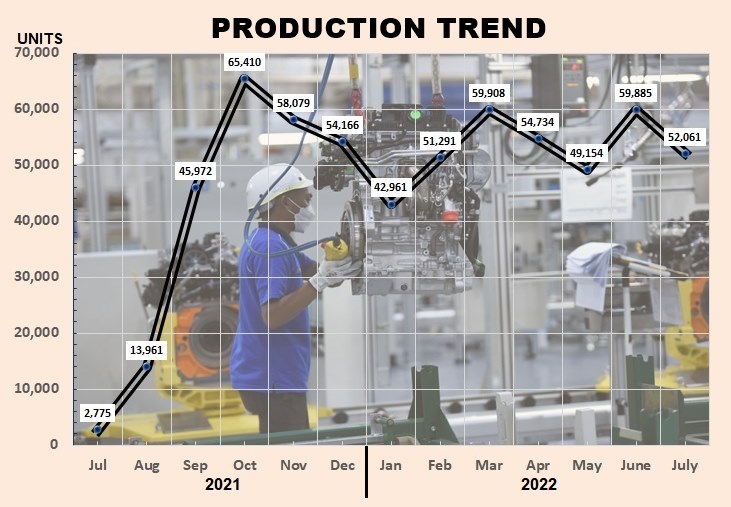

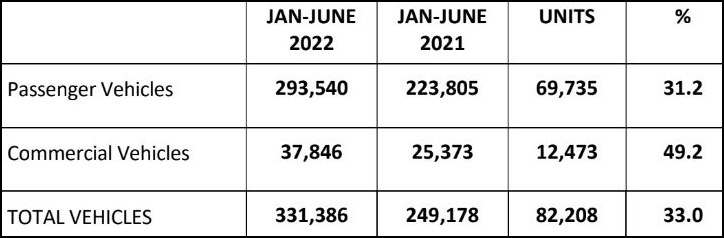

While 2021 was a difficult year for the car companies, 2022 has seen significant increase in volumes in spite of the ongoing supply shortage of certain parts, limiting output from the plants. According to the Malaysian Automotive Association, which has been compiling industry data since 1967, the Total Industry Volume (TIV) in the first six months of 2022 was 331,386 units, an increase of 82,208 units or 33%.

This big increase is attributed to the pent-up demand for new vehicles but it has also to be noted that the TIV for the same period in 2021 was low due to the restrictions of the Movement Control Order (FMCO) in June 2021. As can be seen in the chart, the strict restrictions saw a sharp drop in sales.

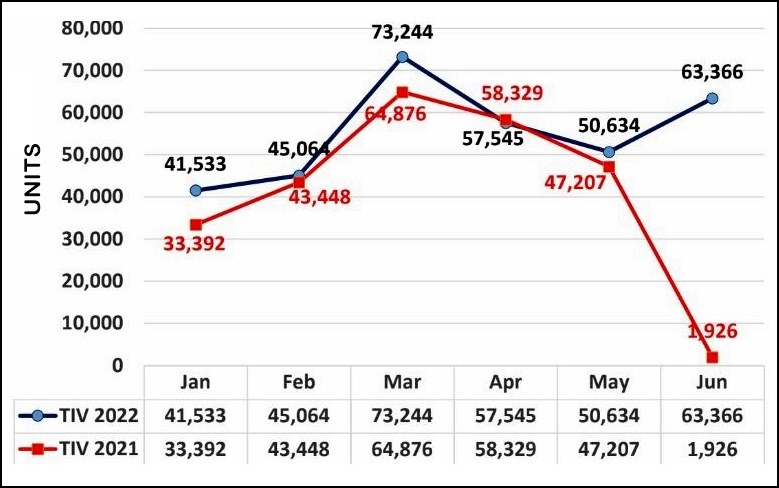

Total Industry Volumes – 2022 vs 2021. All charts provided by Malaysian Automotive Association.

Following the government’s decision of not extending sales tax exemption incentive for passenger vehicles (under the PEMERKASA+ package) after June 30, 2022, bookings surged as those who wanted to beat the deadline rushed to place bookings for new vehicles. Although they would not get their vehicles before the deadline, the government has allowed the exemption to be allowed provided the new vehicles are registered by March 31, 2023.

TIV (Total Industry Volume) of new vehicles by month.

This pushed the June TIV to 63,366 units, an exceptionally high volume as companies rushed whatever stocks they had to customers. The figure could have been higher, had there not bee the shortage of vehicles due to the shortages of chips and components which affected certain makes.

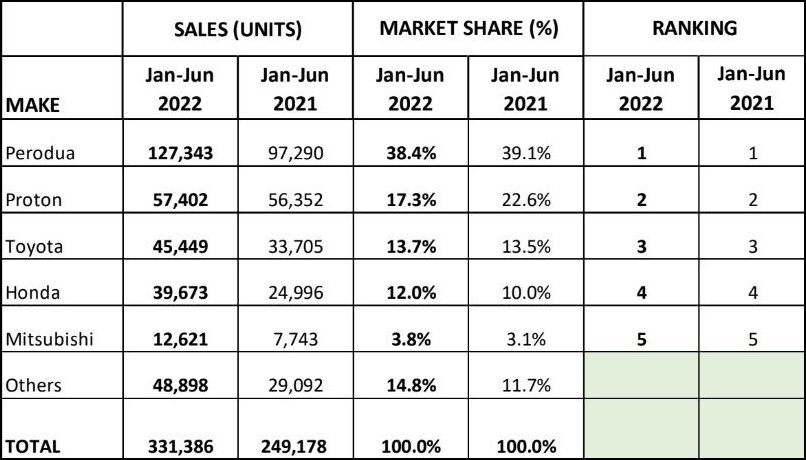

The top 5 brands

The top 5 brands retained their 2021 ranks, with Perodua still leading. While volumes rose, the markets shares of Perodua and Proton decreased, but the market shares of the non-national makes rose.

Higher output from factories

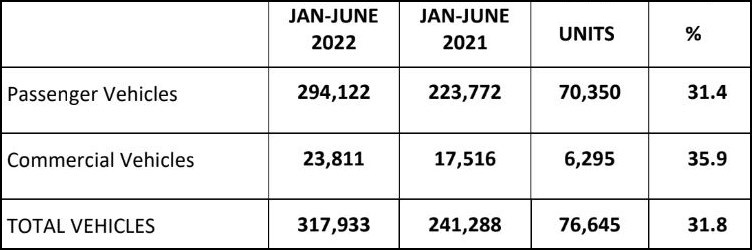

Total production volume in the first half of 2022 also increased likewise by 31.8% to reach a total of 317,933 units compared to 241,288 units in the same period last year. The much higher total production volume seen this year was because there was a total lockdown enforced by the government in June 2021 which shut down factory operations. In addition, the higher output was also in response to the high demand.

Production volumes for first half of 2022 and 2021.

Forecast revised upwards

For the whole of 2022, the MAA has raised its forecast to 630,000 units in view of the strong and positive market trend. This is 30,000 units more than the original forecast announced at the beginning of the year. This means that during the second half of the year, monthly saves will have to be at least 49,760 units.

Revised forecast for 2022. *: Original forecast was announced in January 2022.

In revising its forecast, the MAA has taken various economic and environmental factors into account as well as drawn on input from its members. The association expects the country’s economic recovery to maintain its momentum and the Finance Ministry is maintaining its official GDP forecast of 5.3% to 6.3% for 2022.

However, there are still some factors that can slow the economic growth, such as geopolitical tensions, escalating oil prices, inflationary concerns, and increases in food prices. These may also make consumers hesitate in making purchases, while business in the auto industry may faced increased logistics and shipping costs and experience supply chain disruptions. Bank Negara Malaysia’s recent decision to increase the Overnight Policy Rate (OPR) by 25 basis points to 2.25% may also dampen consumer confidence.

Looking ahead till 2026…. assuming that there are no major disruptions in Malaysia or globally.

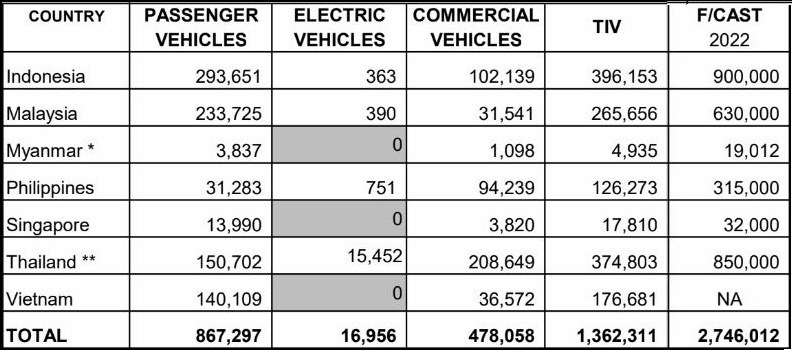

Sales figures in other ASEAN markets from January to May 2022. The data for electric vehicles is based on officially reported numbers by members of the respective automotive associations in each country.

With electric vehicles (EVs) constantly in the news these days, you will by now be familiar with the main selling points: zero emissions and lower maintenance costs. Apart from governmental pressures, the industry is doing its best to persuade motorists to switch from vehicles with internal combustion engines (ICE) to EVs as quickly as possible to build up the numbers and reach economies of scale that can bring production costs down.

Understanding that driving range and price are key factors in consumers’ minds when considering an EV, they are working hard on those factors which will require greater manufacturing innovation and efficiencies across the sector. But the angle of zero emissions from EVs being able to address climate change and preserve the environment is not applicable everywhere. In the more economically advanced countries, ‘saving the planet’ may be something people can also think about (and do something about) but for much of the world, saving themselves first is a higher priority than changing to a more expensive EV in place of their still-functioning ICE vehicle.

“The reality is that, despite EVs eliminating tailpipe emissions, they also produce a ‘long tailpipe’ of increased demand for electricity and energy-intensive materials,” notes a report by global technology company Hexagon. The report, based on original research conducted by Wards Intelligence, says that many of today’s EVs have been designed for short-term well-to-wheel benefits without considering their ‘whole-lifecycle’ environmental footprint.

For motorists, the perspective is only from tank (the fuel tank or battery pack) to wheel whereas a true examination of the benefits of EVs must consider the much bigger picture. While EVs can certainly give the benefits which we are being told about, the cost of making them and running them is a side of the story which consumers don’t ask or know about. But it is one which is generating debate and which suggests that EVs are not necessarily the best solution to addressing climate change.

Bigger picture than just well-to-wheel

An EV can certainly beat an ICE vehicle on emissions while in use but what about over its entire life-cycle – starting with making it and also the resources to give it power? While the ‘well-to-wheel’ analysis typically looks at all emissions related to fuel production, processing, distribution, and use when comparing EVs to ICE vehicles, it is also necessary to cover an even wider scope which includes manufacturing of EVs and end of life.

This is where things start to look different and while studies have found that the amount of carbon dioxide (CO2) in the production and distribution of ICE vehicles and EVs is not significantly different, the battery packs needed in EVs tip the scales.

EVs may have less parts than ICE vehicles but the numerous electronic systems are made from rare earth elements. Making each battery pack (below) also generates a lot of carbon dioxide.

Apart from requiring depletable rare metals, it is estimated that up to 150 kgs of CO2 are released for every 1 kiloWatt hour (kWh) of battery capacity. To provide an EV with 500 kms of range would require a battery that currently has at least 60 kWh of storage capacity. To make such a battery pack would mean that another 9 tonnes of CO2 would be added to manufacturing the vehicle and this is a negative impact from the perspective of environment-friendliness (compared to making an ICE vehicle).

‘Sustainability’ is also touted as another selling point of EVs but if so many of the electricity-generating plants are coal-powered, would it not then be a case of shifting demand of one depleting fossil fuel (oil) to another (coal)? After all, both fuels are the product of dead plants and dinosaurs and other organic stuff that was buried up to a billion years ago. According to a group at Stanford University, the world’s coal reserves will last only till 2090, oil reserves will run out by 2052, and natural gas by 2060. And this is based on current consumption; if demand for electricity starts to rise rapidly with more EVS in use, then the depletion will naturally accelerate.

Half of the planet’s coal-powered electricity plants are in China but in other countries, there are also other types of environment-friendly power generators like wind turbines (below).

Of course, not all sources of electricity use coal or oil. Studies show that 36.7% of global electricity production comes from nuclear or renewable energy (solar, wind, hydropower, wind and tidal and some biomass), with the remaining two-thirds from fossil fuels. But of these two-thirds, 54% of the electricity generators are in China alone where the world’s biggest car market is.

Less parts, less complexity but…

EVs are also described as being ‘less complex’ as they have less parts than ICE vehicles. They are essentially computers with electric motors and wheels. But a closer examination will show that all those electronic parts – which are in greater numbers than in ICE vehicles – are composed of more ‘high-end’ materials – lithium, cobalt and rare earth elements which need to be mined. The rare earth elements have to be extracted and waste from the processing methods can be radioactive water, toxic fluorine, and acids.

Estimates of lifetime emissions from EVs depend not just on mileage travelled in the vehicle’s lifetime but must also take into account whether the battery pack will last equally long. Current lithium-ion technology for battery packs has degradation over time, and after hundreds of charge/use cycles, become less effective. Like the battery in mobilephones, the lifespan will vary but studies have found that it takes at least 1,000 full cycles before the battery pack starts to show any degradation.

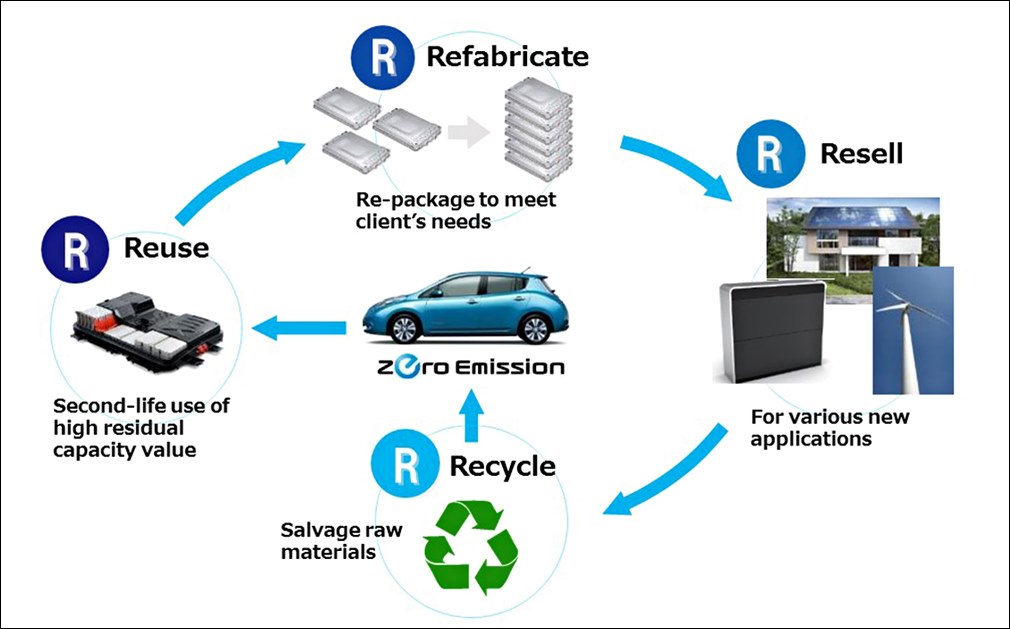

Nissan is one of the carmakers that has started a project to recycle end-of-life battery packs which can still serve as energy storage units in other applications.

Eventually, it will probably be that entire EVs – including their battery packs – will have a specific lifecycle so a new battery pack is unnecessary. Everything can be recycled and the batteries might even serve a further purpose for other equipment. The latter process already exists in some places through projects initiated by manufacturers.

The true test of success for electric vehicles is therefore to deliver on their broader promise and create a commercially successful automotive industry that can also be environmentally sustainable. The Hexagon survey demonstrates that manufacturers are aware of the need to go beyond eliminating end-user emissions and improve the ‘whole-lifecycle’ sustainability of EVs. Carmakers and suppliers also increasingly recognize the need to think beyond the vehicles and instead build car parts for a second life and a circular economy.

This will require the industry to compress and connect manufacturing processes together so that sustainability is ‘baked in’ to a vehicle’s DNA at design stage and every part is conceived and created to support both a sustainable car and economy.

EV assembly at the Polestar factory in China.

The automotive industry is therefore caught between bottom-up consumer expectations and top-down political pressure for more sustainable EVs. “Living up to the lofty vision of an ethical and environmentally-friendly automotive industry means moving beyond simply eliminating tailpipe emissions to creating lighter, more sustainable materials and manufacturing methods. Emerging smart manufacturing approaches are vital to bring these innovations to market within demanding deadlines, while remaining profitable,” said Paolo Guglielmini, President of Hexagon’s Manufacturing Intelligence division.

So should you buy an EV?

The ‘dark side’ of EVs aside, the change will come about and even if you presently have the choice of staying with an ICE vehicle, your children probably won’t. EVs are the future and ICE vehicles will either be banned from use in some countries or their sale will be stopped so that they eventually diminish in numbers (which could take decades in places like Malaysia). Right now, for Malaysians, it would be a good time to buy an EV if you can afford one because of the duty-exemption. This exemption won’t be around forever although there may be other incentives in future though not as great as this one.

There are definitely advantages to owning and using an EV compared to an ICE vehicle. Running and maintenance costs are less but you will incur an extra initial expenditure setting up a charging point at home (if you can do so). The earlier disincentives like limited range are steadily being erased as battery technology improves and the same goes for recharging facilities. The network is steadily growing and with increasing numbers of EVs on the roads, there will be more justification to invest in expanding the network.

Like computers and mobilephones, the technology keeps advancing each year. As we said earlier, there is a race on by the industry to improve range and reduce costs and so performance will get better and as volumes rise, production costs can go down so EVs will become cheaper. In this case then, perhaps it may be a better idea to consider the subscription approach instead of the outright purchase and ownership model that has been the norm for decades. This will help you to remain current with the latest technologies by changing cars regularly without concerns about depreciation and disposal.

General Motors (GM) was the market leader in the US market since 1931 but last year, its place was taken not by Ford, Chrysler or even Tesla but by a foreign brand – Toyota. The Japanese carmaker reported sales of 2.332 million vehicles in 2021, beating the 2.218 million units that GM announced the same day. A year earlier, GM had still held No.1 spot with 2.55 million units while Toyota did 2.11 million units, and Ford reported 2.04 million units.

Understandably, Toyota has not played up on its ascent to No.1 position – the first foreign carmaker to do so – since it can be a sensitive issue among Americans. Although it imports many vehicles, it also has huge factories in America that manufacture a number of models there, so they are as American as those from the Big Three with substantial local sourcing of parts as well, not to mention being made by American workers.

But Toyota, like other Japanese carmakers, has been through periods of consumer resentment for their products and at one time, were even forced to voluntarily limit exports from Japan in the 1980s. Starting with a limit of 1.68 million cars (total for all makes) in 1981, the voluntary export restraint brought on by US political pressure remained for some 9 years. While it relieved some pressure on the American carmakers, it also resulted in foreign carmakers setting up factories in America so they could build their cars there, behind the ‘barrier’ and unrestricted by quotas.

The Crown was the first Toyota to appear in the USA in 1958. The carmaker established its first operations in California, from where it would spread across the country and then begin setting up factories to make its cars there as well. 63 years later, it has become the No.1 carmaker in the country, displacing GM which held the title for 31 years.

Besides the COVID-19 pandemic which affected the whole auto industry, there were also serious supply chain issues and more disrupting, a shortage of semiconductors for the many electronic systems in today’s motor vehicles. Every manufacturer was affected but some, like Toyota, had managed to plan well, which the Japanese are good at. Lessons learnt from the tsunami/earthquake disaster in Japan in 2011 also helped Toyota to have good management of its supply chain and to ensure sufficient buffer stocks for any major disruption.

No plans to boast about title

Toyota doesn’t plan to use its achievement in promotions and instead highlights other sales achievements in 2021 (in the US market) like selling the most electrified vehicles for the 22nd consecutive year, being the No.1 retail brand (which excludes leasing and fleet sales) for the 10th consecutive year, No. 1 in passenger car market share for 10th consecutive year, and the bestselling models in the passenger car category (Camry), midsize SUV category (Highlander), SUV category (RAV4) and small van category (Sienna).

The Honda Accord was the first foreign model to become the No.1 passenger car sold in America in 1989. But the Camry has taken the position most years since 1994, and has been No.1 for the past 20 consecutive years. The success of the model was, in part, due to the refusal of the top guys at Toyota USA to take the model designed in Japan which was too conservative. With the support of the Toyodas, they managed to get the chief engineer to come up with a completely different design which, in some ways, mirrored the Lexus LS400 that had become a benchmark in the US premium luxury class from 1989.

While the Honda Accord was the first foreign model to be the bestselling car in America in 1989, it’s been the Toyota Camry (1994 model shown below) which has been No.1 for the past 20 consecutive years.

The RAV4 is also another great success story for Toyota in America. It appeared at just the right time as Americans had a growing love for SUVs. Small and as easy to drive as a passenger car, it was ideal for the transition from a passenger car to SUV. It virtually created a new category overnight which would influence the rest of the industry to start following. Three years after the RAV4 appeared, Lexus also did a similar thing in the premium segment with the RX300.

The RAV4 created a new market segment almost overnight when it appeared in 1995. Since then, it has been a top-seller in its class.

Electrified models fuel sales

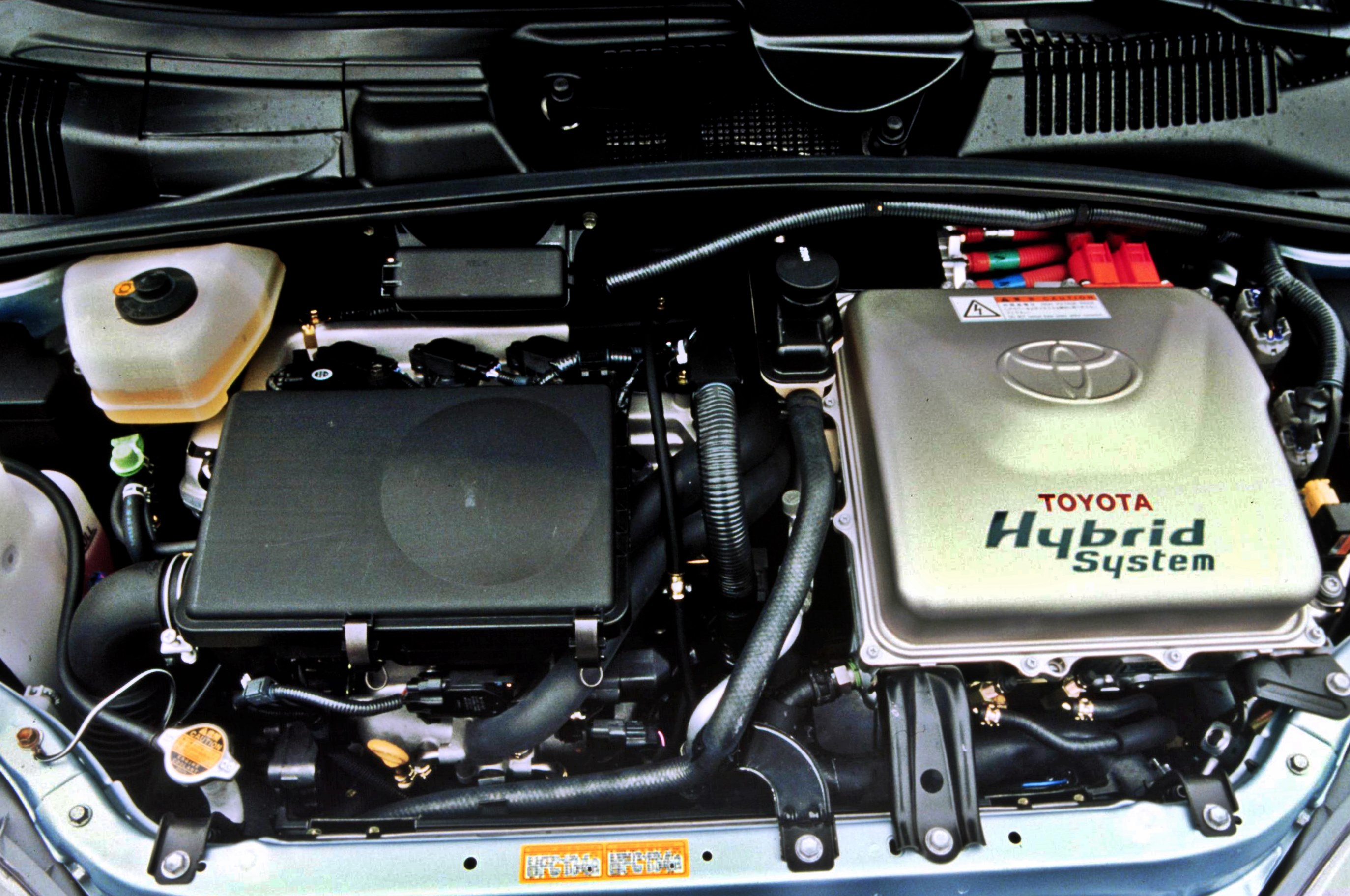

In recent times, Toyota’s growth has been fuelled by electrified vehicles, which it has been selling since the late 1980s when it introduced the Prius as the world’s first mass-produced vehicles with a hybrid powertrain. Since then, the range of hybrid models has expanded and it has even started selling a fuel-cell electric vehicle called the Mirai. Last year, electrified models accounted for about 25% of the total vehicles Toyota sold, up 73.2% in volume from a year before.

The Prius was the first mass-produced vehicle in the world with a hybrid powertrain when it was launched in 1989. Since then, Toyota has expanded its range of electrified models with hybrid powertrains and the picture below shows the models sold in the USA in 2013.

The total industry volume was just under 15 million vehicles in 2021 and 2022 is expected to see growth. Some forecasts put it at just over 15 million, but Toyota is more optimistic and thinks it could reach 16.5 million units, of which it is aiming to contribute 2.4 million. Whether GM will regain its crown remains to be seen although, like Ford long ago, the carmaker realizes that it is not much point chasing a No.1 title at the expense of profitability. Toyota somehow has managed to grab the No.1 position while still remaining profitable, though, but the Japanese are always conscious of a rival overtaking them so they never stop looking in the mirror.

The Malaysian auto industry, like many other industries in the country, has been badly impacted by the measures taken to fight the COVID-19 pandemic since last year. Representing the new motor vehicle distributors, assemblers and manufacturers, the Malaysian Automotive Association (MAA) commends the government for its efforts to contain the spread of the coronavirus in order to save lives.

However, the MAA feels the Enhanced Movement Control Order (EMCO), Phase 1 and Phase 2 of National Recovery Program approach needs to be reviewed and re-considered, especially for key economic states like Selangor, Wilayah Persekutuan Kuala Lumpur, Perak, Johor, Penang and Negeri Sembilan. The EMCO approach had been enforced in Selangor and WP Kuala Lumpur for more than 2 weeks now while some states have transitioned into Phase 2 of the NRP.

Whole supply chain affected

“The whole supply chain in the automotive sector has been seriously affected particularly by the complete shutdown of operations in EMCO states/localities like Selangor and WP Kuala Lumpur. Feedback received from many of our members indicated that business operations – even in non-EMCO states – are hampered due to disruptions in the supply chain”, said Datuk Aishah Ahmad, President of MAA.

During the EMCO stage, not a single business activity from the automotive sector is allowed to operate, while for states under Phase 1 and Phase 2 of the NRP, the vehicle showroom and distribution centres are still not allowed to operate despite the opening up of most of the other economic sectors.

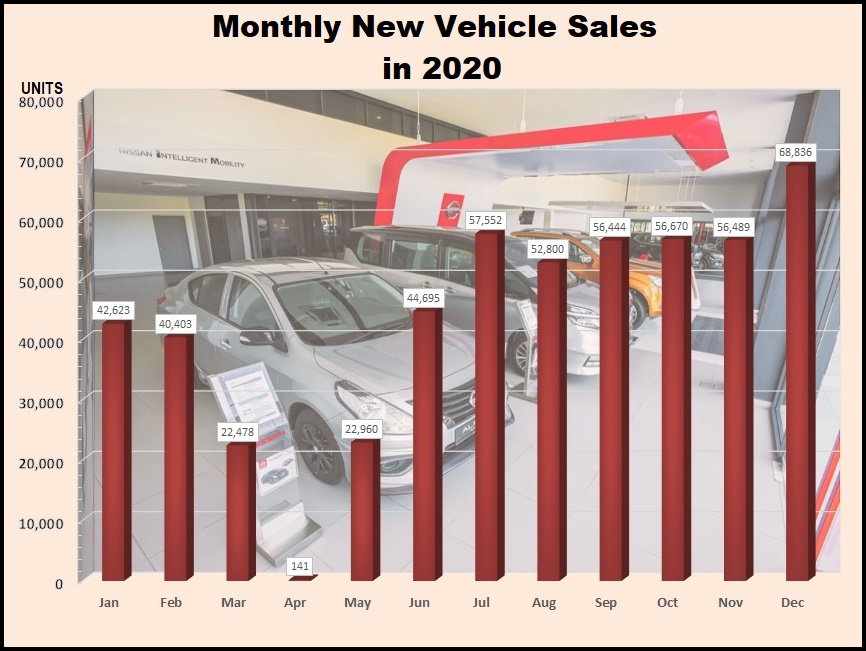

Production and distribution of automotive products (motor vehicles, components and parts) and sales of vehicles have been halted since June 1, 2021. The stoppages of all these activities will have far-reaching implications to the entire automotive ecosystem nationwide. In April last year, sales and production plummeted to almost zero when the first MCO was in force.

Implications of continuing closures

While automotive companies may suffer from loss of revenue, profitability, export markets and closure of businesses, their employees face issues such as pay cuts, loss of income (particularly for sales personnel) and even retrenchment in certain cases. The government will also lose in terms of lower revenue collected from excise duties, import duties, sales taxes and road taxes for motor vehicles.

The closures of automotive workshops and parts centres in EMCO states/localities such as Selangor and WP Kuala Lumpur will not only cause inconvenience to all vehicle owners in general but may also endanger those whose vehicles may have defects or problems. Failure to repair faulty parts in such vehicles can pose a serious risk to all road-users. These include vehicles which may be belonging to frontliners such as those in the PDRM, Ministry of Health, etc. who may encounter damages or breakdown in the course of doing their work.

With factories and distribution centres (for vehicles and parts) in EMCO states/localities unable to operate, this will disrupt the supply chain to business operations in states/areas under Phase 1 and 2 of the National Recovery Plan (NRP). As a result, the recovery efforts by the government will be negated.

Increasing damaged inflicted

The consequences arising from stoppages of the automotive factories, workshops, and distribution centres (for vehicles and spare parts) in EMCO states/localities is indeed very serious, the MAA stresses. The longer these facilities do not operate, the greater the damages inflicted on to the automotive industry in particular, and the country in general.

The MAA is therefore appealing to the government to allow automotive sector activities (workshops and distribution centres for passenger and commercial vehicles and spare parts) to operate with immediate effect albeit at certain capacity and with strict SOPs in place in states under EMCO, Phase 1 of NRP and Phase 2 of NRP.

Selangor and WP Kuala Lumpur account for close to 50% of Malaysia’s total industry volume of new vehicles each year. Many of the key automotive companies for both production of vehicles and components are located within these two states. In addition, some MAA members also have their sole and or central distribution centre (for vehicles and spare parts) located within the Klang Valley.

In addition, to reduce congestion at ports, the MAA is proposing to allow a window of two to three days per week for receiving and storing cargos for the automotive sector similar to what was practiced during MCO 1.0 last year. The Malaysian automotive industry is heavily dependent on the domestic market. Export markets exist but are insufficient to sustain the industry.