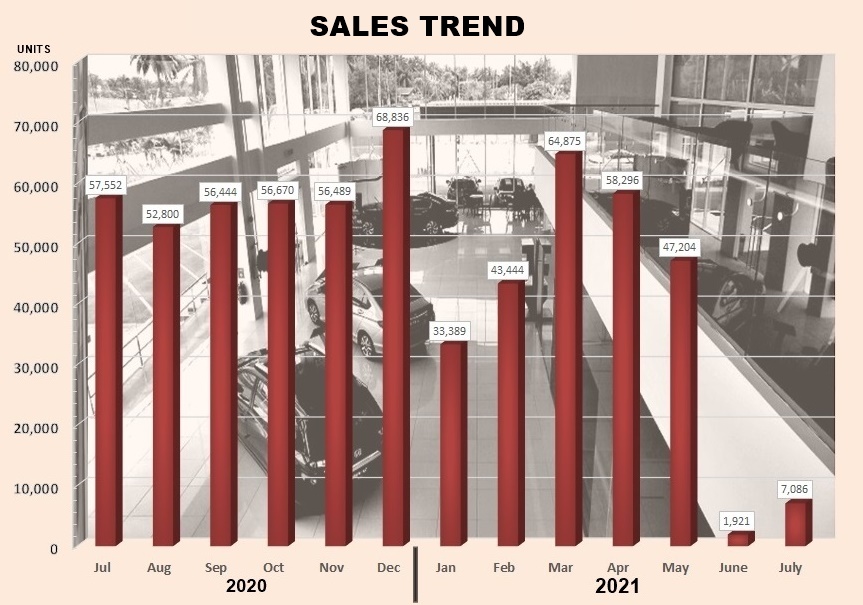

As expected, new vehicle sales in July 2021 were way down, though not as rock-bottom as June when the Total Industry Volume (TIV) was under 2,000 units. As in June, the continued closure of showrooms meant that no sales could be conducted and even if they could, registering the vehicles would not be possible. However, July’s TIV was 270% or 5,465 units higher as showrooms could operate in Sabah and Sarawak so sales were possible there and accounted for the higher numbers.

Minimal bookings from online channels

According to the Malaysian Automotive Association (MAA), which has been compiling data since the 1960s, members reported that bookings via online channels were minimal. These ‘virtual showrooms’ started to appear over the past year as stricter SOPs were in force and there was also concern that customers might not be comfortable coming to showrooms. Customers can make bookings and make payments via online transfers to at least start the process. However, there are still the other things like loan applications which still need some personal interaction.

The cumulative TIV after 7 months reached 256,215 units this year, which was about 10% higher than for the same period in 2020 – and this has been with 2 months of virtually no sales. With sales resuming from mid-August, there will be a backlog to clear plus new orders so the TIV by year-end might still be higher than for 2020.

3-digit production figures

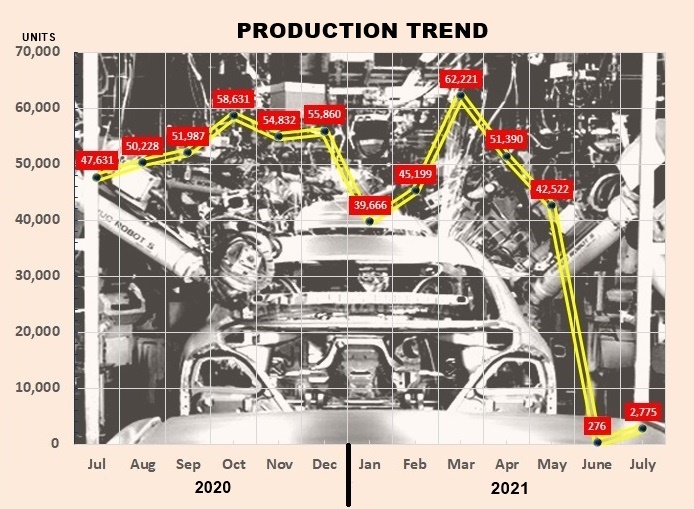

On the production side, the assembly plants have had to suspend operations too and the output fell to three digits in June but rose again in July. The disruption has been challenging for the plants which very much prefer consistent assembly. The shortage of microchips is also slowing output and as the end of the year nears, pressure will be on to deliver as many vehicles as possible because car companies are using the sales tax exemption as a selling point. It expires at the end of this year so many will want to make sure they can enjoy those savings.

Will sales pick up again?

Looking ahead, the MAA expects August sales to be better although there are only two weeks to the end of the month for sales. Furthermore, given the current situation in the country, not only with the pandemic but also the political situation, consumer sentiment may be cautious, and people will be reluctant to spend a lot.

According to MAA President, Datuk Aishah Ahmad, total losses for the local auto industry for the months of June and July have been estimated to be more than RM14 billion. “This is just only from sales of vehicles in the domestic market. Our members also lost much in terms of revenue from exports of vehicles and components, and sales of spare parts locally. All in all, these losses had been very substantial and unprecedented”, she said.

Car showrooms, accessory stores and carwash centres can resume operations from August 16

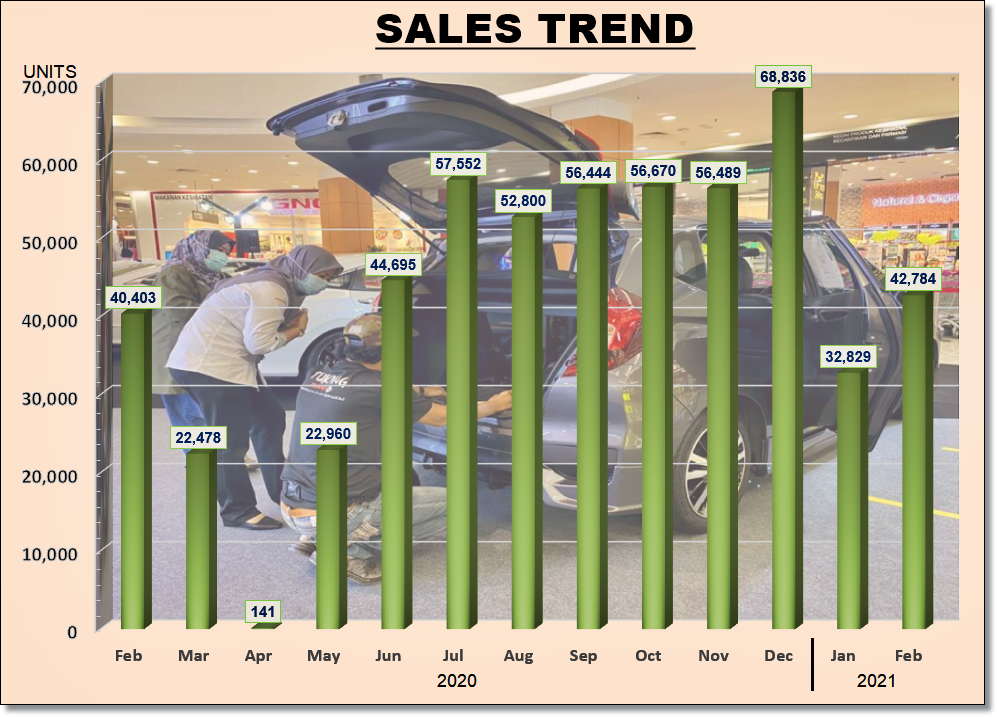

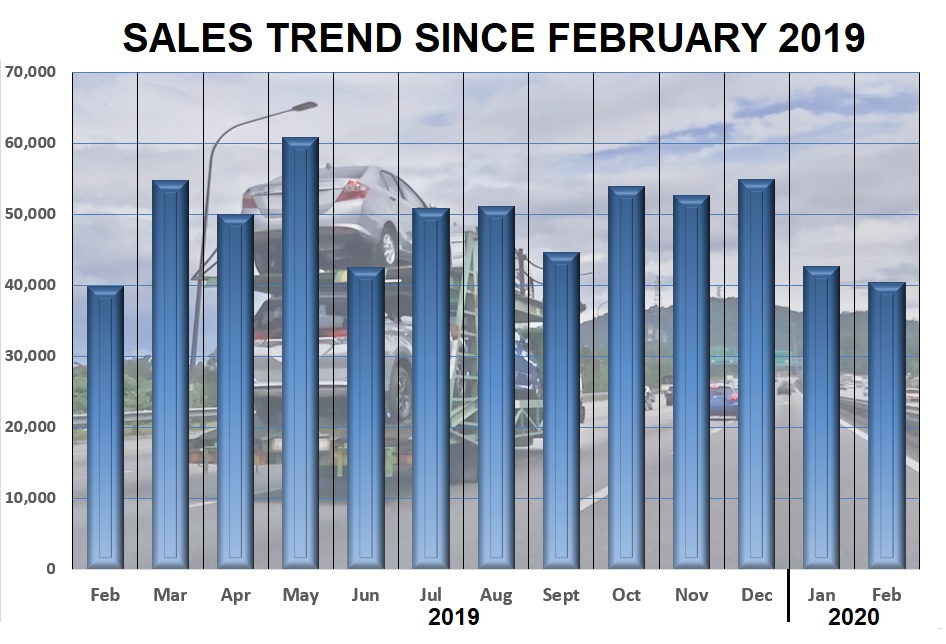

After a slow start to the new year, new vehicle sales jumped 30% in February as the buying mood returned, pushing the Total Industry Volume (TIV) to 42,784 units. Of this number, 4,861 units were commercial vehicles )including pick-up trucks). The segment volume was 30% higher than last year, possibly because a year ago, concerns about the pandemic were growing and businesses would have suspended purchases as a precaution.

The higher TIV was also attributed to the easing of the Movement Control Order in some states, making it possible for customers to go to showrooms if they wished. However, many companies have made a big push towards online marketing and have many processes which replace traditional practices where the customers had to personally come to the showroom.

The backlog of orders for some models also contributed to the increase in new vehicles registered in February. Late last year, sales were brisk and popular models were in short supply and just as when there was the GST-free period some years back, the plants could not ramp up production quickly to meet the sudden rise in demand.

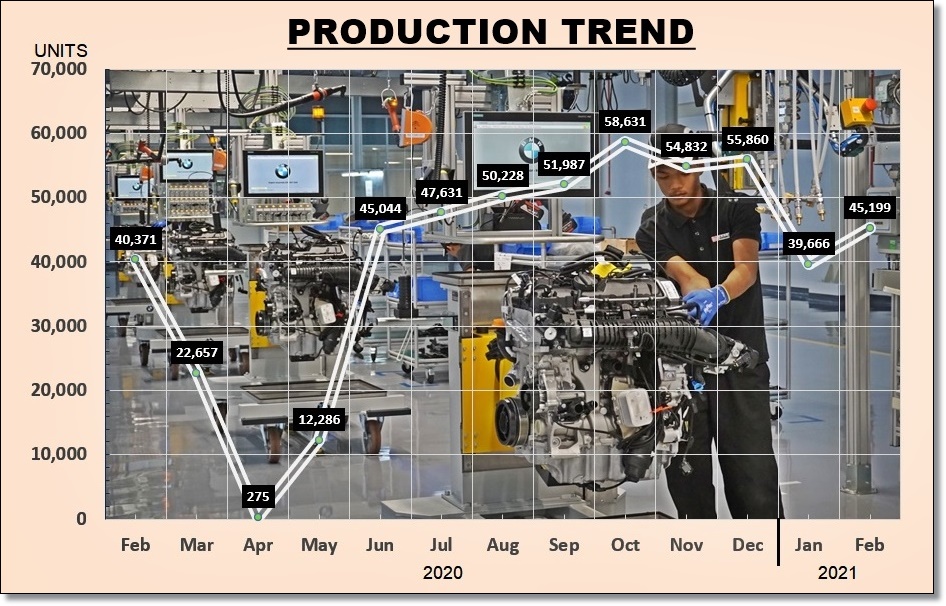

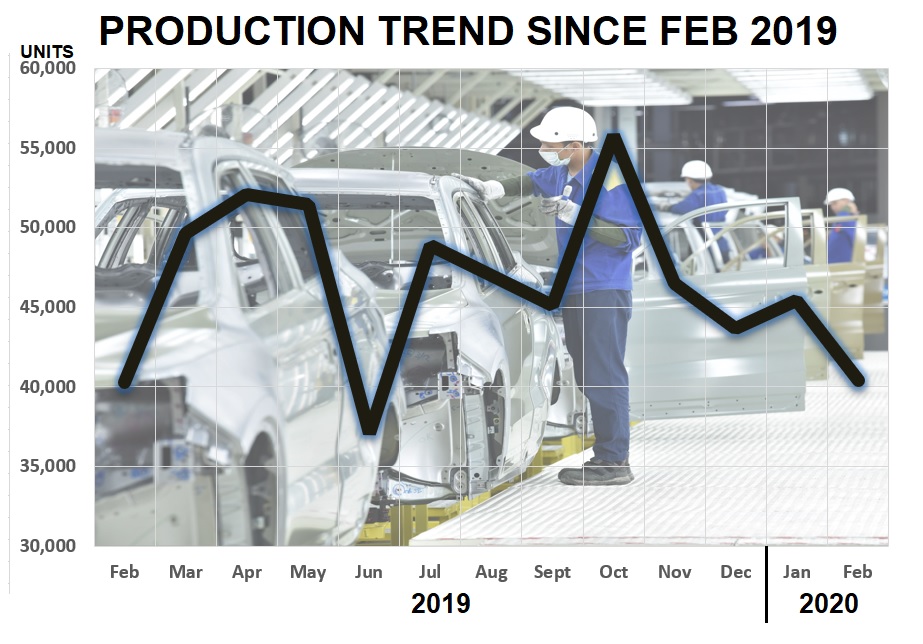

The response from the production side seems to have gained momentum as February output of 45,199 vehicles was a 14% increase compared to January output. And compared to the same month in 2020, the output this year was 12% higher, with commercial vehicles registering a jump of 57%.

For the month of March, it is likely that the TIV will still be climbing, especially if the pandemic situation keeps diminishing in severity and public confidence becomes stronger. March is also the final month for some companies to make the final push to get the best business results for their financial year which ends on March 31.

The appeal of new models being launched will also bring more sales to companies like Perodua which began deliveries of its new Ativa SUV in early March. At the time of writing, we are aware of a couple of other models that will be launched this month too so there should be higher consumer interest which will continue up to the Hari Raya festive period.

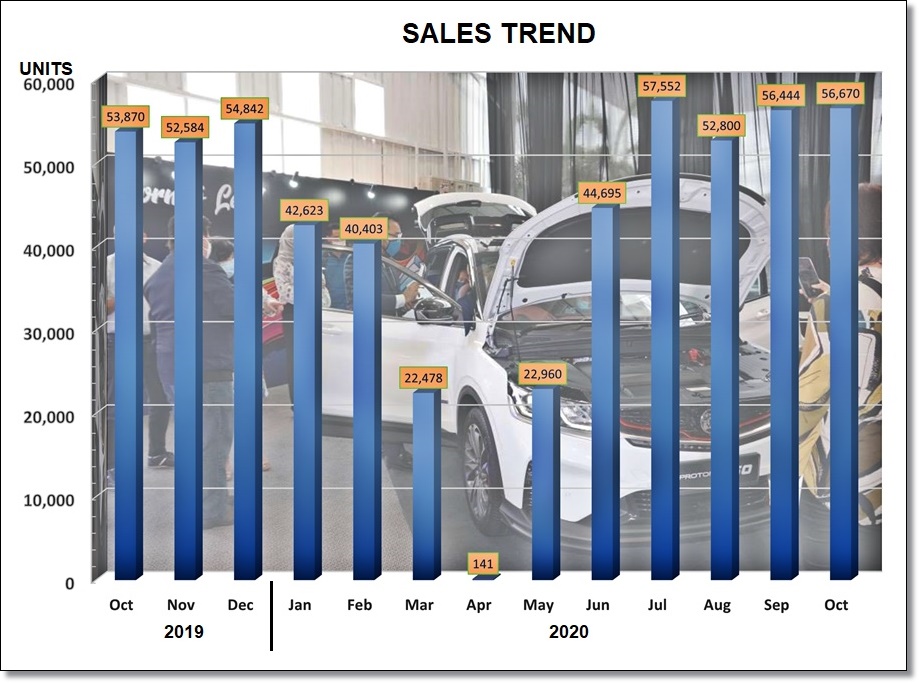

♦ The upward trend seems to have flattened out with October’s Total Industry Volume (TIV) less than 1% higher (226 units) than the TIV for September. No doubt, the reduction in the cost of buying a new vehicle due to the government’s Sales Tax exemption incentive still helps encourage sales and when compared to the same month in 2019, this year was 5.2% better.

♦ The TIV for the period from January to October has almost reached 400,000 units, reached 398,159 units to be exact. With two months remaining to hit the MAA’s 470,000-unit forecast for 2020, can the monthly TIV for November and December average 36,000 units? Since July, it has been above 50,000 units.

♦ Of the 56,670 units registered, 86% were passenger vehicles (excluding pick-up trucks).

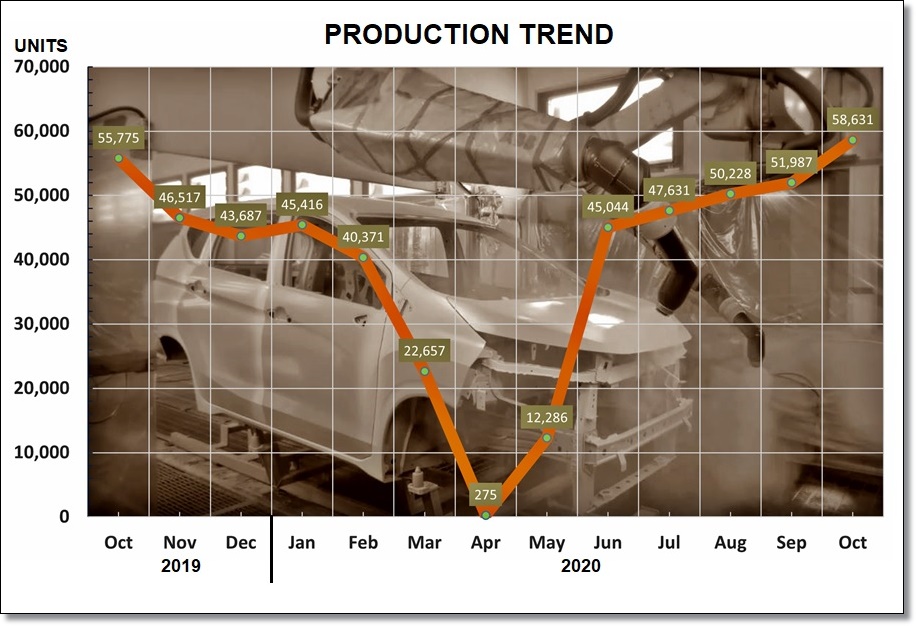

♦ The output from the plants rose more substantially to 58,631 units in October to meet the higher demand and to also build up stocks for the end of the year period. It is likely that December will see a rush to take delivery so as to enjoy the sales tax exemption, This would be unusual as many customers often want to defer to the new year.

♦ One thing that could dampen sales a bit would be the uncertainty surrounding the COVID-19 pandemic. While the government is reluctant to impose a full-scale MCO like what we had in March and April when businesses had to shut down completely, there may be areas where stricter conditions are imposed, especially in the Klang Valley where there is the largest number of vehicles sales.

♦ The MAA does expect some softening of the market in the light of a broader impostion of the CMCO and says that members have reported a slowdown in showroom traffic. Nevertheless, many companies now have online facilities for customers to know more about products and then make bookings as well, so at least the initial phase of transactions has been addressed in the ‘new normal’.

KEY POINTS:

♦ Although the Total Industry Volume (TIV) for the month – 40,403 units – was higher (by 1.5%) than the same month in 2019, it was 5.3% or 2,249 units lower than the figure reported for the month of January 2020.

♦ The total sales of new passenger vehicles was 36,702 units (about the same as last year) while commercial vehicles, including pick-up trucks, was 3,701 units (20% higher than February 2019).

♦ The decline in sales was attributed to delays in launches of new models and consumer concerns about the COVID-19 pandemic which showed signs of worsening.

♦ The Malaysian Automotive Association, which has been compiling data since the 1960, expects that March sales will be lower as the Movement Control Order came into effect around the middle of the month.

♦ Production of new vehicles dipped 11.1% after the upswing in January. As demand could be seen to be slowing down, many companies would have cut output to avoid building up too many stocks.

♦ The total output of 40,371 units during February 2020 was 17% lower than that of the same month in 2019.

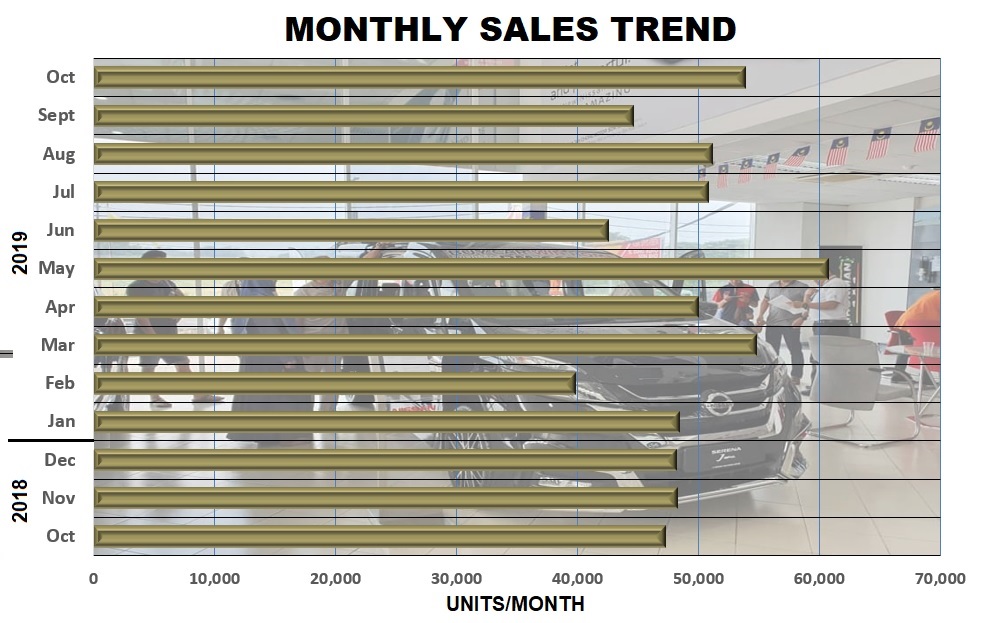

New vehicle sales for October – the first month of the final quarter of 2019 – began on a high note with a 21% increase over the Total Industry Volume (TIV) in September to 53,870 units. This volume was also 14% higher than for the same month in 2018 although a comparison may not be right since it was after the GST-free period when sales had seen a huge boost and the market slowed down in the first few months after that.

The Malaysian Automotive Association (MAA) attributed the increased TIV to more selling days as well as more working days. When there are many holidays, there is also disruption in processes such as registration and loan approvals, delaying completion and affecting deliveries.

By segment, passenger vehicles (excluding pick-up trucks for personal use) accounted for 93% of the TIV in October, a 16% increase over the same month in 2018. However, commercial vehicle sales were virtually unchanged with 4,883 units (including pick-up trucks) delivered.

The cumulative TIV after 10 months of this year reached 496,861 units which was 5,267 units lower than for the same period in 2018. The higher TIV last year was due to the 3-month GST-free period which saw an above-average surge in monthly sales as buyers could enjoy significant savings (especially for the more expensive models).

Production

The assembly plants collectively produced 55,775 vehicles in October, compared to 51,789 vehicles in the same month in 2018. The increase was largely in the passenger vehicle segment while the commercial vehicle segment declined.

Cumulative production for 10 months was 481,816 units which was 97% of the cumulative sales volume but this direct comparison may not be entirely accurate as there would be an overlap in stocks and imports. Popular models may leave the plants within days of being completed but there may also be vehicles which don’t move out so fast (although the plants would not want them around too long either as they take up parking space).

With two months left to the year and a forecast of 600,000 units for the year by the MAA, it means that sales in November and December must average 51,569 units. This year, 5 months have seen the TIV above 50,000 units and it’s often the case that there is such a big boost in December that the forecast is met.