Source: Monthly reports of Malaysian Automotive Association

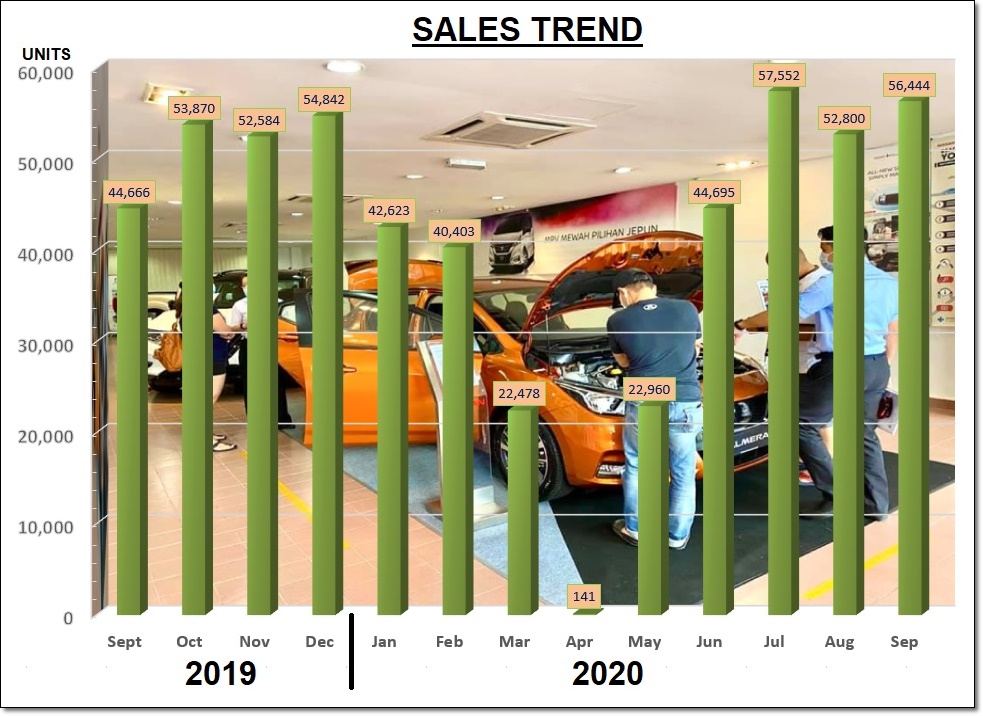

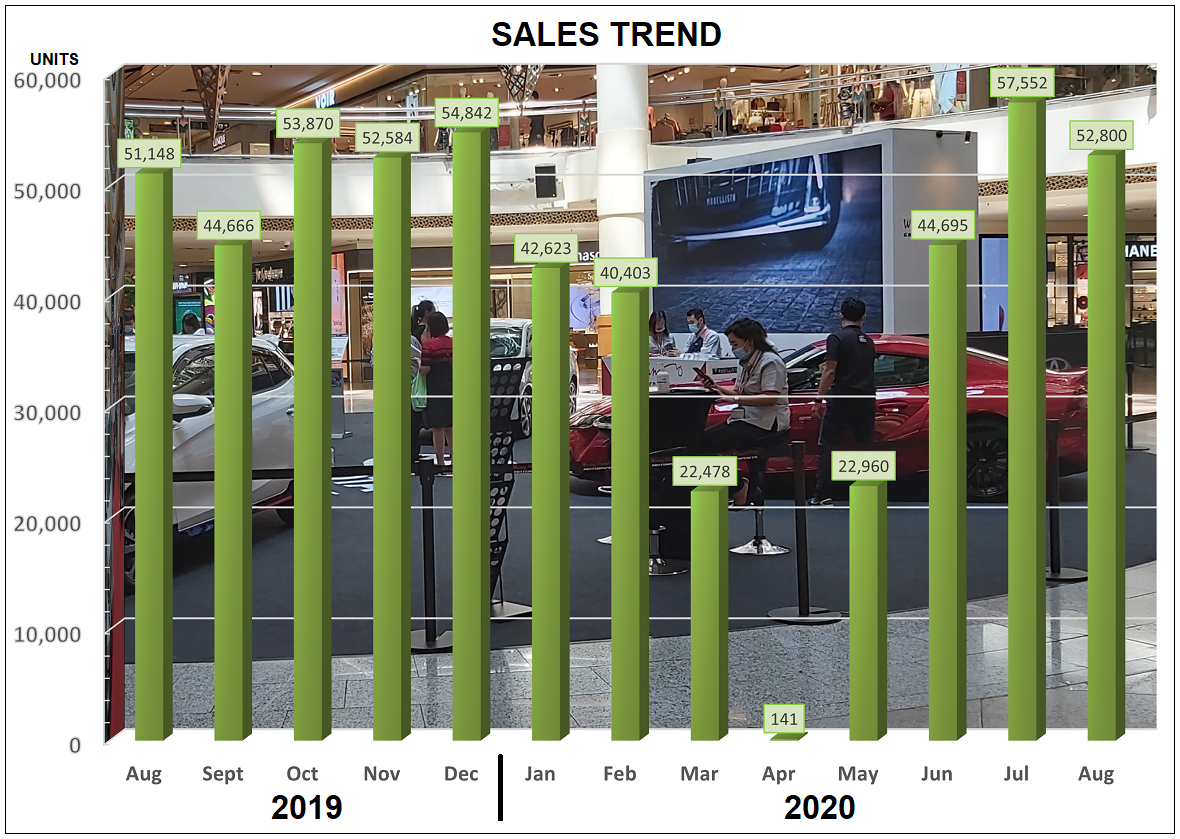

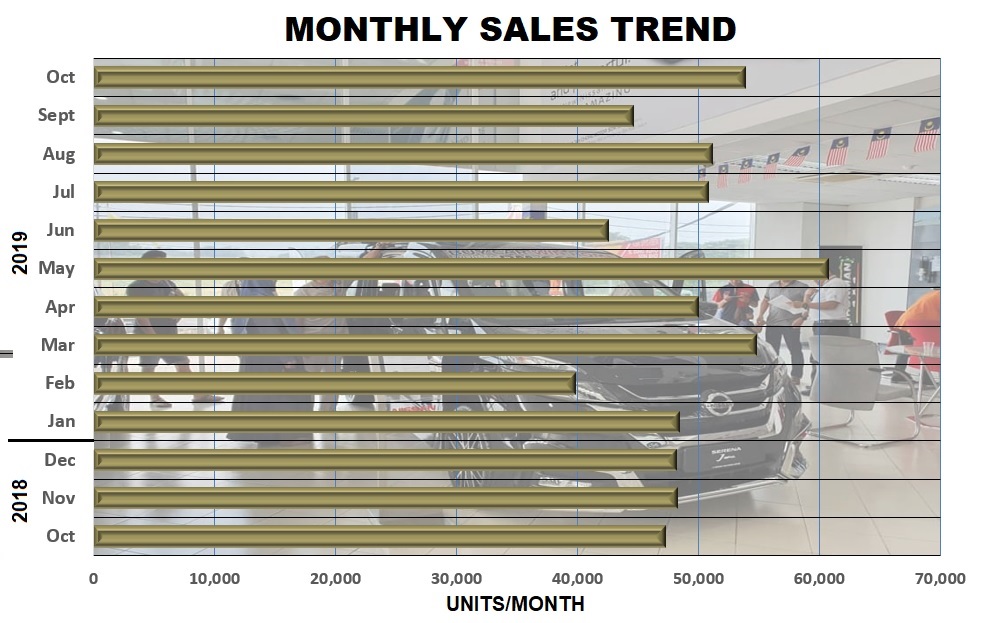

♦ The government’s Sales Tax exemption incentive continued to encourage many to buy new vehicles in September, pushing the Total Industry Volume past 56,000 units. In fact, it was 26% higher than the same month in 2019.

♦ Of the 56,444 units registered, 9.7% were commercial vehicles which includes pick-up trucks.

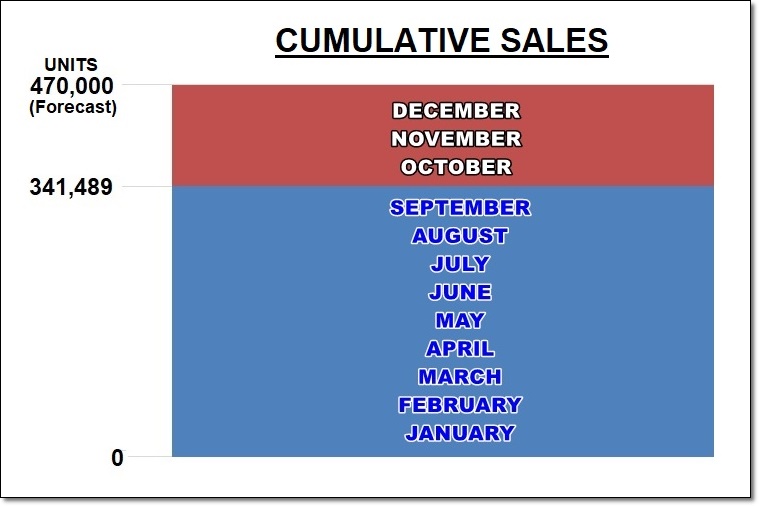

♦ Cumulative sales after 9 months have reached 341,489 units, To achieve the MAA’s 470,000-unit forecast for 2020, the industry must sell an average of 42,837 units in the remaining 3 months. Since July, the monthly sales have been over 50,000 units so the question will be whether this level can be sustained until the end of the year?

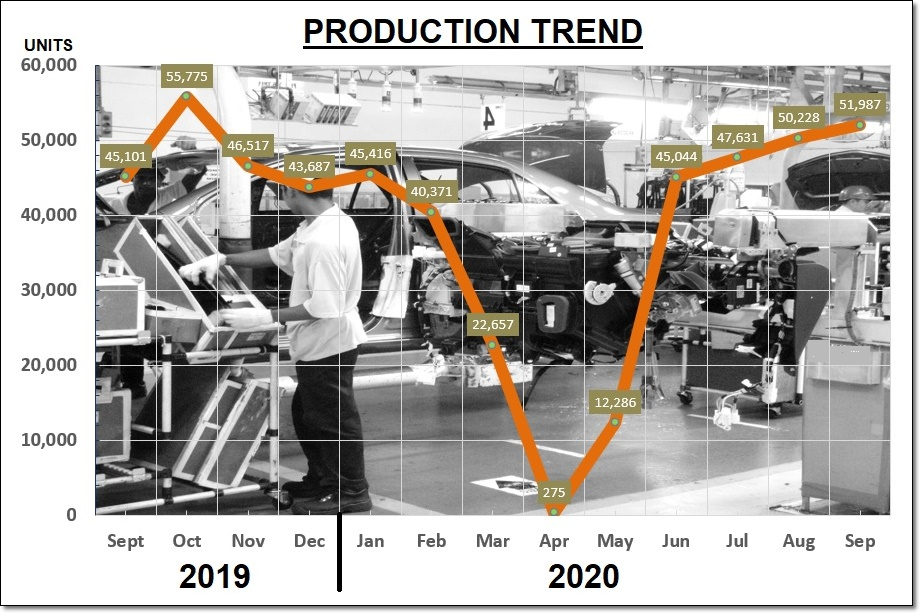

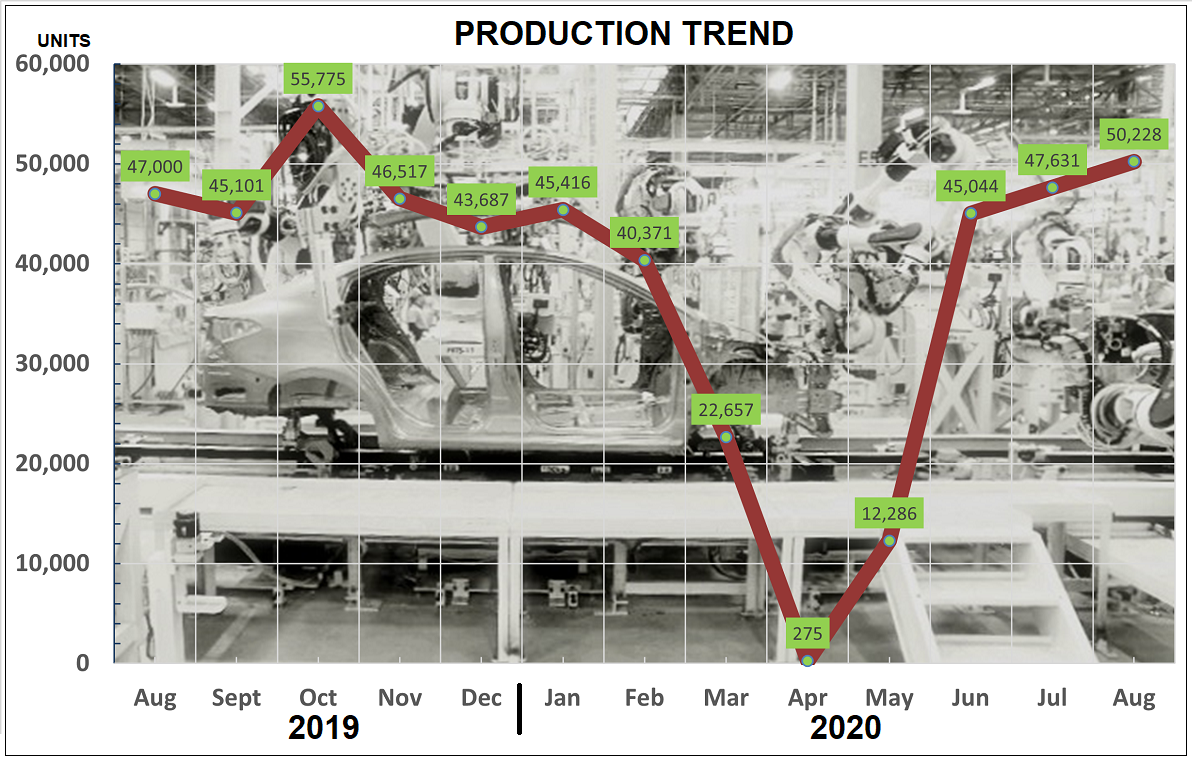

♦ Production rose slightly as most plants assembled as many units as possible to meet the higher demand. The output rose of 51,987 units was 15% higher than the same month in 2019, but output of commercial vehicles was lower by 26%.

♦ October numbers could be lower as the burden of making monthly instalments has resumed with the cessation of the loan moratorium that was provided by the banks as a form of assistance during this pandemic period. Furthermore, the imposition of the CMCO for two weeks in the month (if not longer) in the region with the most new vehicle sales may have an effect too. However, unlike the situation in March when all car companies had to suspend all activities, businesses can presently continue operating and relevant government agencies also process new vehicle registrations.

Source: Monthly reports of Malaysian Automotive Association

♦ It should be noted that the sales volume shown for August does not indicate the Total Industry Volume (TIV) as some companies have chosen not to share their data on a monthly basis and will only do so on a quarterly basis.

♦ Although the August sales volume was 8% lower than July’s, the government’s Sales Tax exemption incentive continued to help boost sales as the same month in 2019 registered 3% lower sales.

♦ Cumulative sales after 8 months have reached 285,045 units, 28% lower than for the same period in 2019 but a slightly narrower gap compared to the January – July period for both years.

♦ To achieve the MAA’s 470,000-unit forecast for 2020, the industry must sell an average of 46,238 units in the remaining 4 months. The 52,800 units sold in August were therefore above that level but can high volumes be sustained till the end of the year?

♦ Production rose again as the plants could resume normal production capabilities and respond to the increased demand. The output rose by 5.4% to 50,228 units which comprised 47,934 passenger vehicles and 2,294 commercial vehicles. However, the loss of almost 3 months of production has put the cumulative output 31% behind that of 2019 in the same 8-month period.

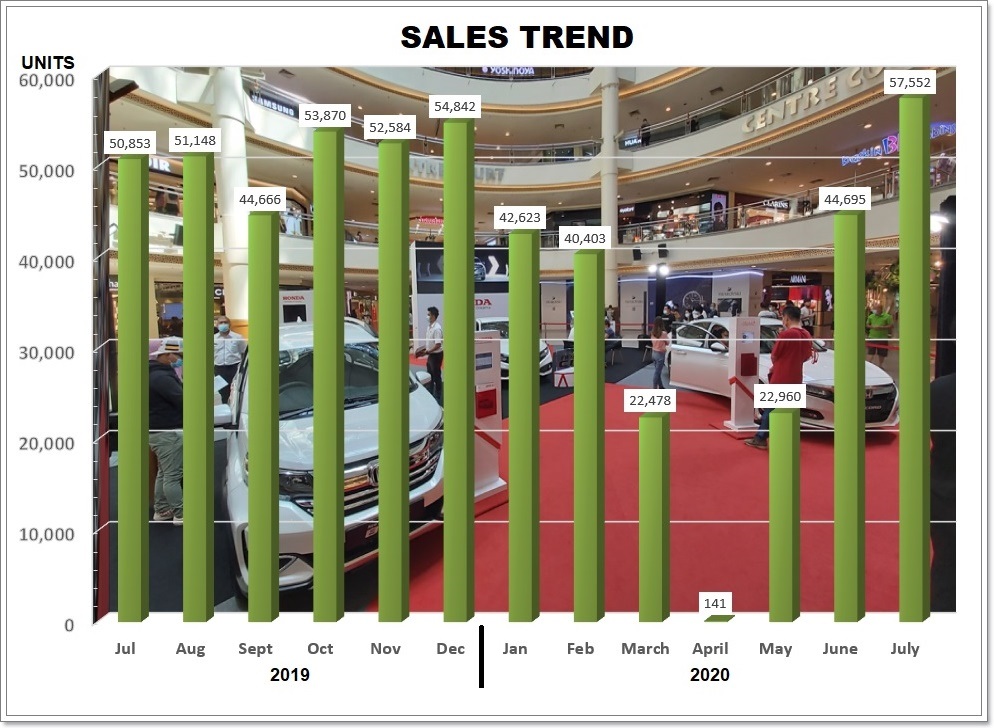

♦ With the government exempting Sales Tax and car-buyers able to save money, new vehicle purchases have started rising, with July increasing by 29% over the June Total Industry Volume.

♦ The Total Industry Volume (TIV) of 57,552 units comprised 52,119 passenger vehicles, and 5,433 commercial vehicles (including pick-up trucks).

♦ Compared to the same month in 2019, this year’s volume was 13% higher.

♦ However, cumulative sales after 7 months of 232,245 units are 33% lower than for the same period in 2019 which was 347,171 units.

♦ To achieve the MAA’s 470,000-unit forecast for 2020, the industry must sell an average of 47,551 units, or a total of 237,755 units, in the remaining 5 months.

♦ Production also rose as plants shifted into higher gear and compared to the same month in 2019, the total output was only 3% lower. Cumulative production is, however, 36% lower than for the same period last year.

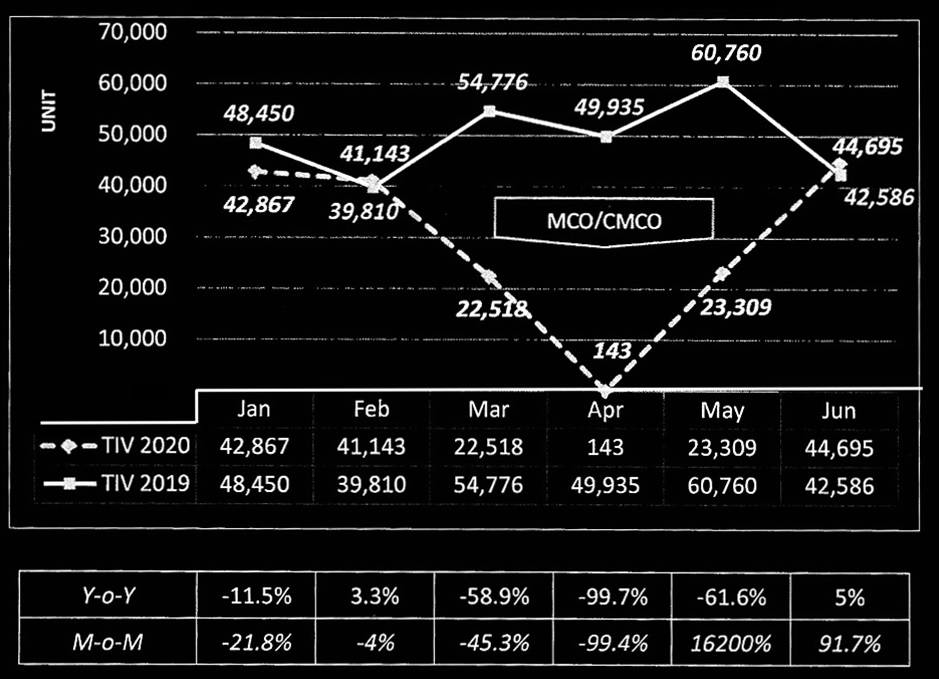

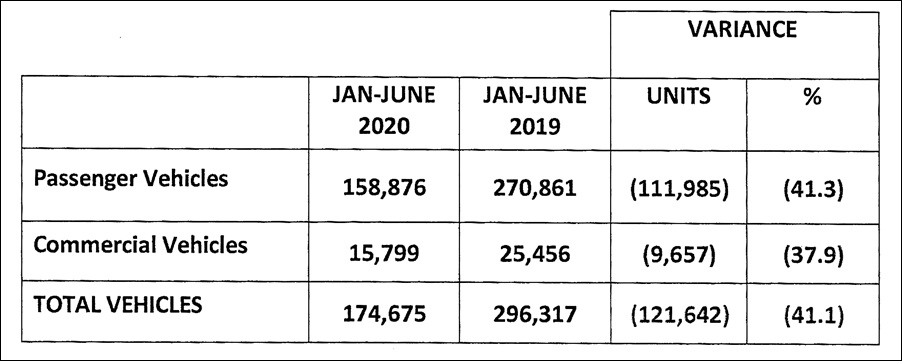

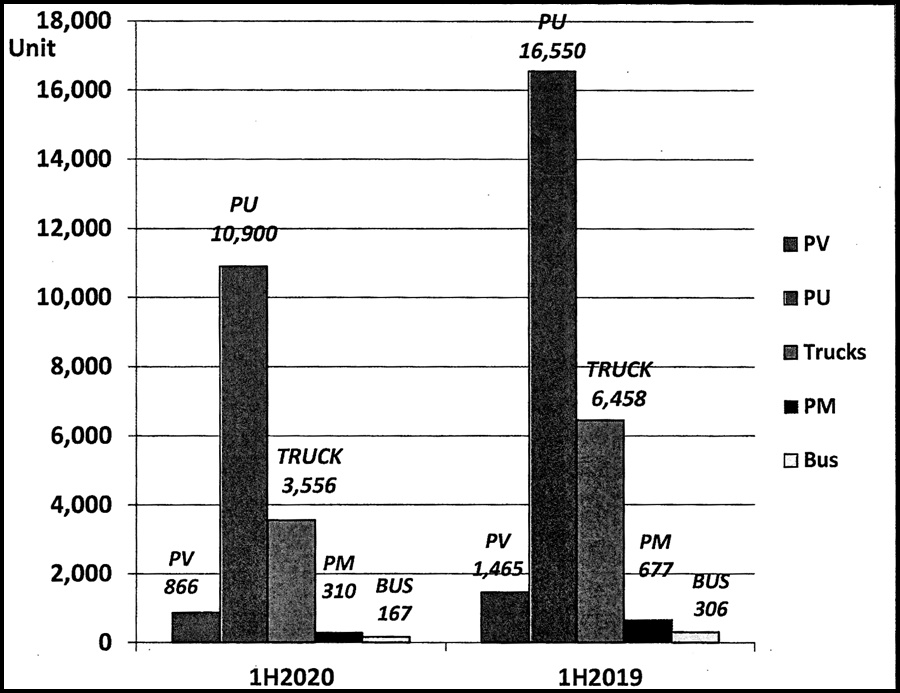

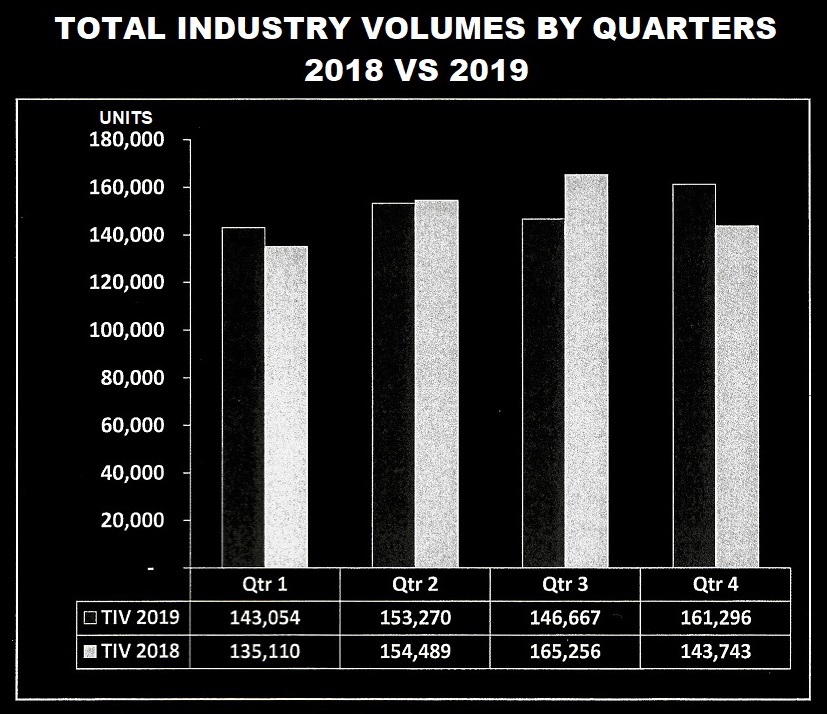

The official numbers are out and as expected, they show a grim picture of the auto industry’s performance in the first 6 months of this year. For the first half (H1) of 2019, the Total Industry Volume (TIV) was almost 300,000 units but this year, it fell by 41.1% to 174,675 units.

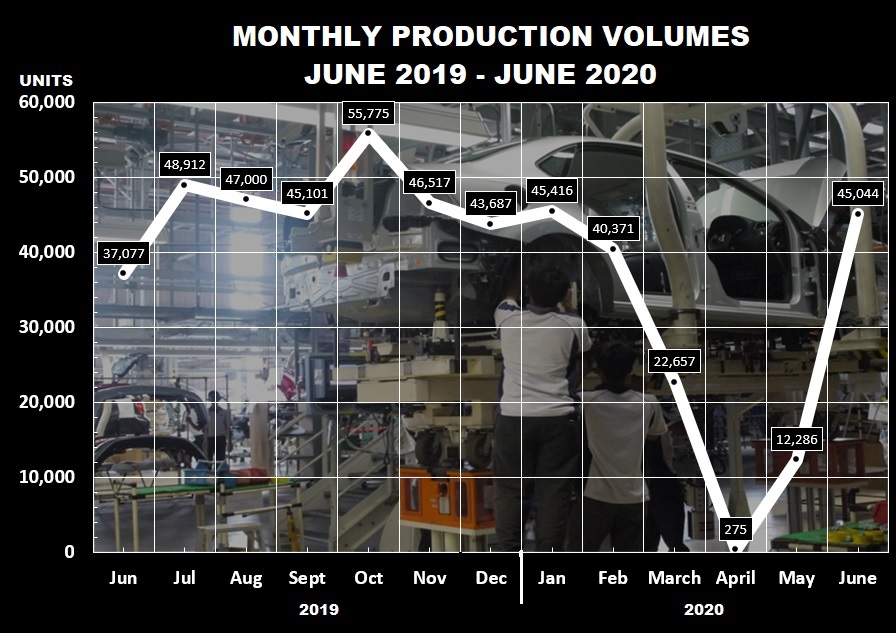

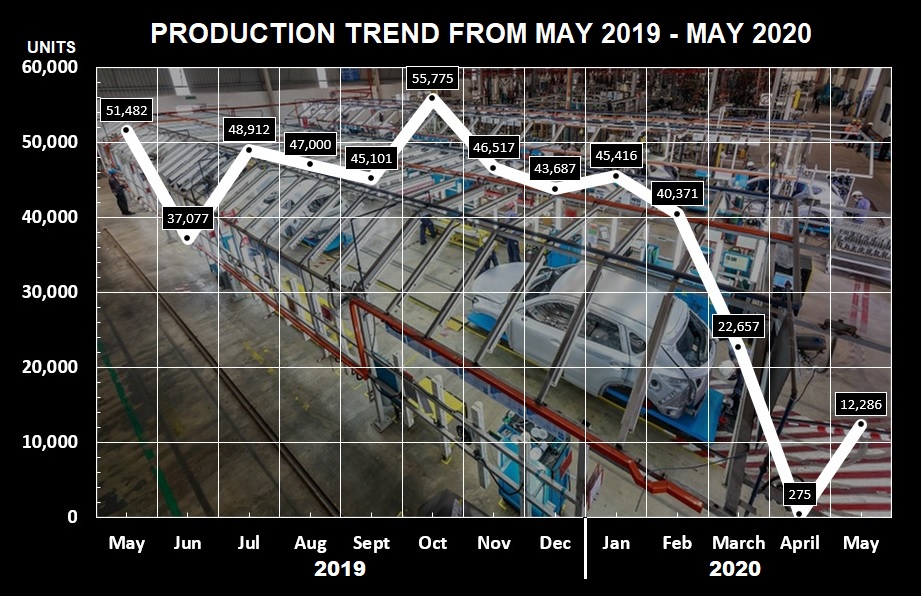

As the chart shows, the unprecedented contraction started in March when the Movement Control Order (MCO) was implemented in the middle of the month and the slide continued through April with a 99.7% drop compared to April 2019 as no business could be done. By May, the situation shows signs of improvement that the government was willing to relax the MCO and allowed many businesses to resume operations, with strict Standard Operating Procedures (SOPs) to be observed.

The resumption began with service centres and factories and then showrooms were also allowed to open for business. While large numbers of customers didn’t visit showrooms, many companies began to promote their online services for booking which at least started the purchasing process without having to physically be in contact with the customer.

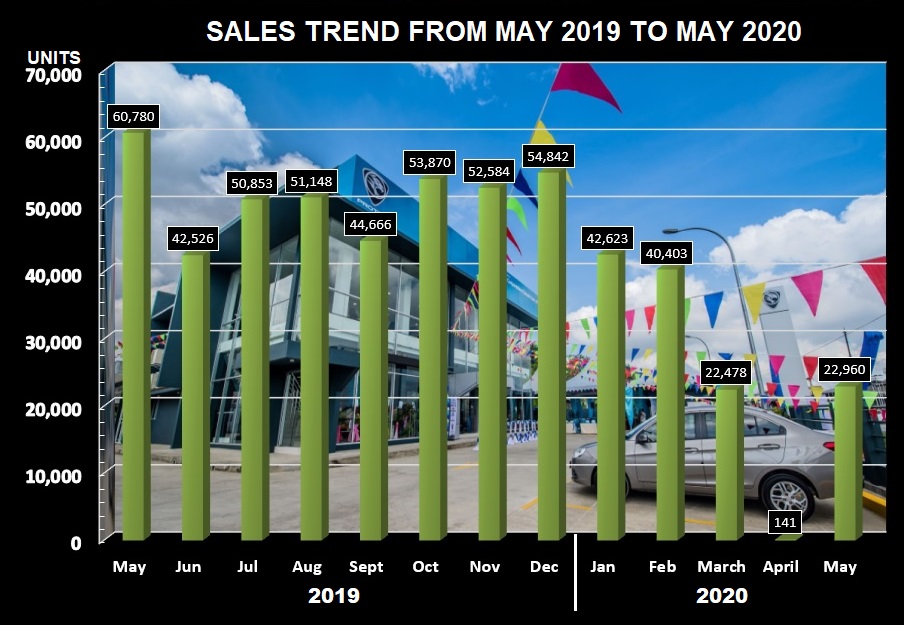

May saw a climb in numbers to 23,960 units and then came some good news that was part of the government’s plan to help industries recover: the sales tax of 10% would be exempted from June 15 to December 31, 2020. For locally-assembled models, which make up the dominant share of new vehicles sold, the exemption would be 100% and for imported CBU models, it would be 50%. It was hoped that the lowering of prices would encourage people to buy new vehicles.

Like passenger vehicle sales, commercial vehicle sales also fell this year but pick-ups continued to have the biggest volume.

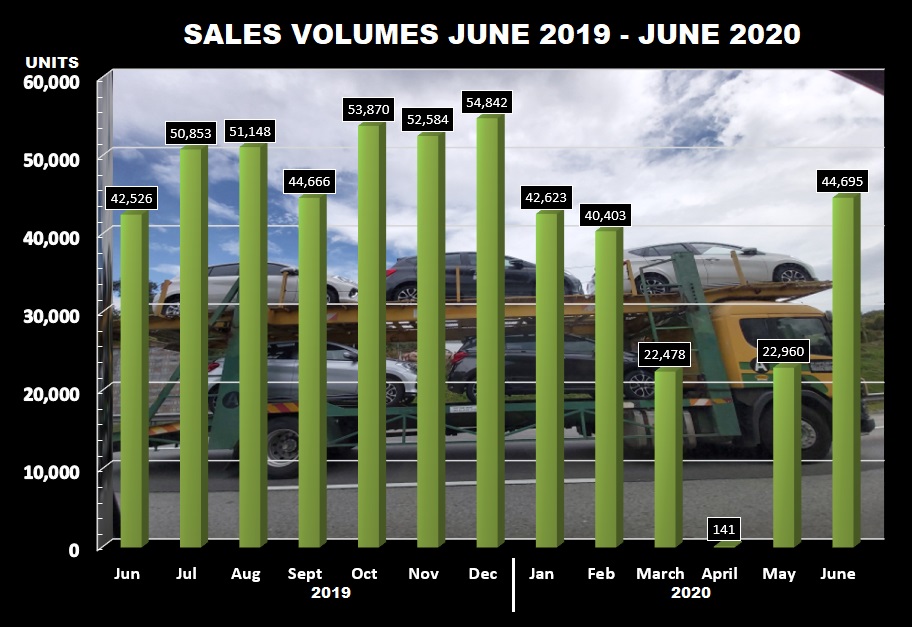

Even with just two weeks in June when the prices were reduced (although Perodua started adjusting prices downwards a bit earlier), sales shot up by 91.7% from the May TIV to 44,695 units – even higher than the 42,526 units reported in June 2019.

2020 forecast revised twice

When the MCO was in force and its impact on the industry was clear, the MAA revised its forecast for the year downwards to 400,000 units. Then, when the government announced the exemption of sales tax, the forecast was revised again as it was felt that the auto industry-specific incentive, along with other economic incentives, would help to boost sales. The revision saw the TIV for 2020 going up to 470,000 units.

This means that, for the second half of the year, the TIV would have to be 295,325 units or almost 50,000 units each month. That may appear a bit ambitious but last year, 5 of the six months in the second half of the year saw volumes over 50,000 units. However, consumers were uncertain about the economy then, not their lives; it is different this year with concerns about COVID-19. Many people have lost their jobs (the unemployment rate increased to 5.3% in May from 3.3% in February) or had big pay cuts and buying a new vehicle might be one of the last things on their mind.

Used car business booming

The used car industry is experiencing a boom, though. According to MAA President, Datuk Aishah Ahmad, apart from wanting to spend less on a vehicle purchase (or not at all), many people may be reluctant to use public transport to avoid risks of infection and therefore buy a low-priced used car for their transport needs.

Obviously, the auto industry would like more assistance from the government to help in its recovery but understandably, the government has to help other industries as well. The new National Automotive Policy (NAP) which was announced at the beginning of the year has yet to be implemented and the MAA will soon be meeting MITI to get more clarification on the policy as well as to offer suggestions on how the industry can be helped in its recovery. The MAA President thinks that the policy is unlikely to be changed despite the challenging economic conditions.

Other ASEAN markets

As always, the MAA press conference also included an overview of how other ASEAN markets are doing and as would be expected, there was a big drop in the total regional sales and production volumes by 42% and 39%, respectively. Only Myanmar did not have a decline in sales (in fact, its sales increased by 5%) during the first 6 months of 2020 but that market is small – less than 8,000 units over a 5-month period. Compared to the 5-month period in 2019, production in Thailand and Indonesia, the two big markets which also export substantial numbers of vehicles, dropped by 40% and 33%, respectively, while Malaysian production was 51% down.

After 2020

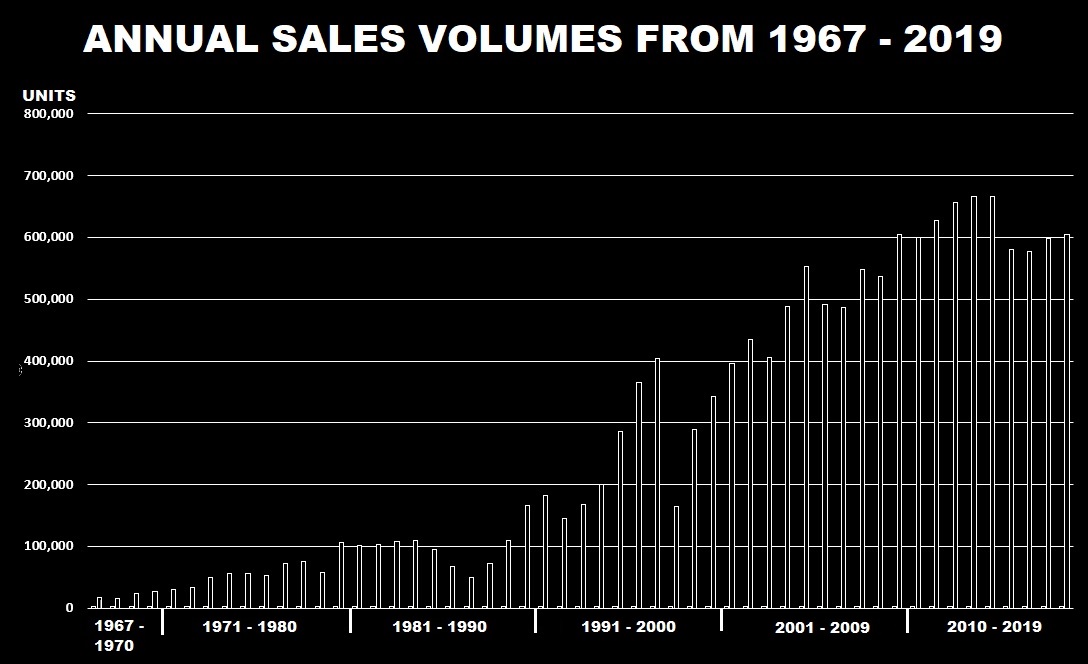

The MAA’s forecast for the next few years is conservative and as the TIV for 2020 is going to be lower than normal – the last time it was around 470,000 units was in the early 2000s – 2021 is expected to see a 17% increase to 550,000 units. However, after that, the TIV may slow down and a 9.1% increase to 600,000 units is forecast for 2012. Thereafter, it may be just 2% a year till the end of 2024.

At this time, it’s hard for anyone to say with certainty how things will be. As the International Monetary Fund (IMF) has said, ‘the trajectory of the pandemic remains hard to predict’. Unlike economic recessions where business drops but when things get better, it picks up and continues to grow. This pandemic situation is like a world war, with devastation including loss of lives as well, that impacts virtually everything and with the economies so interconnected, every country will be affected.

Note: Some companies are reporting on a quarterly basis so the Total volumes for April and May are not finalised. Source: Malaysian Automotive Association.

♦ After the unprecedented fall in sales for April due to the shutdown of all operations, new vehicle sales rose as activities were allowed to resume in May. However, the JPJ only began registration processes from May 13.

♦ The Total Industry Volume (TIV) rose by 22,819 units, comprising 20,456 passenger vehicles, and 2,504 commercial vehicles (including pick-up trucks).

♦ Cumulative sales after 5 months reached 129,561 units, about half the volume for the same period in 2019.

♦ To achieve the MAA’s revised 400,000-unit forecast for 2019, the industry must sell 270,439 units in the remaining months, or an average of 38,634 units.

♦ Production also rose again but compared to the same month in 2019, the total output was 76% lower.

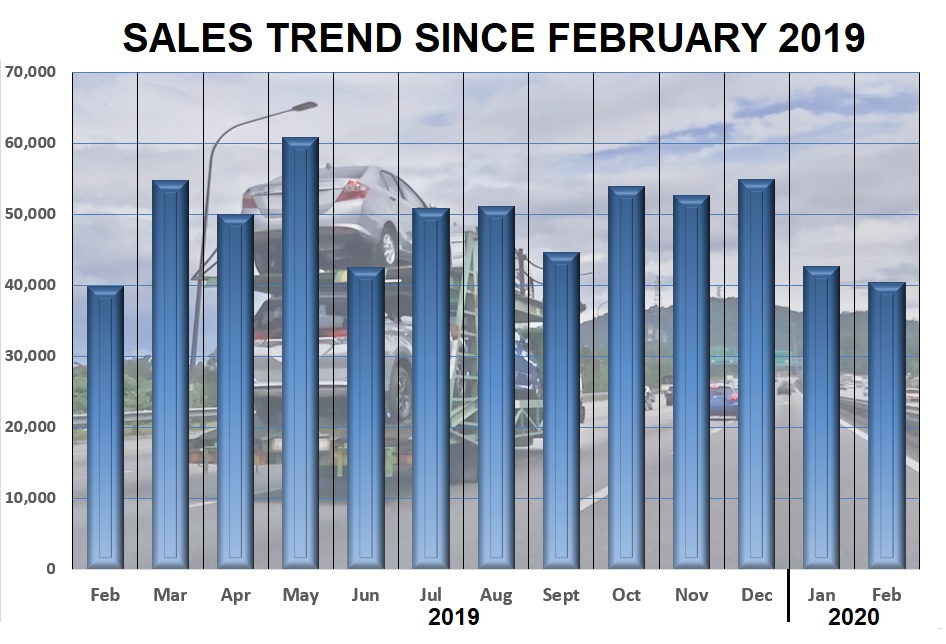

♦ Although the Total Industry Volume (TIV) for the month – 40,403 units – was higher (by 1.5%) than the same month in 2019, it was 5.3% or 2,249 units lower than the figure reported for the month of January 2020.

♦ The total sales of new passenger vehicles was 36,702 units (about the same as last year) while commercial vehicles, including pick-up trucks, was 3,701 units (20% higher than February 2019).

♦ The decline in sales was attributed to delays in launches of new models and consumer concerns about the COVID-19 pandemic which showed signs of worsening.

♦ The Malaysian Automotive Association, which has been compiling data since the 1960, expects that March sales will be lower as the Movement Control Order came into effect around the middle of the month.

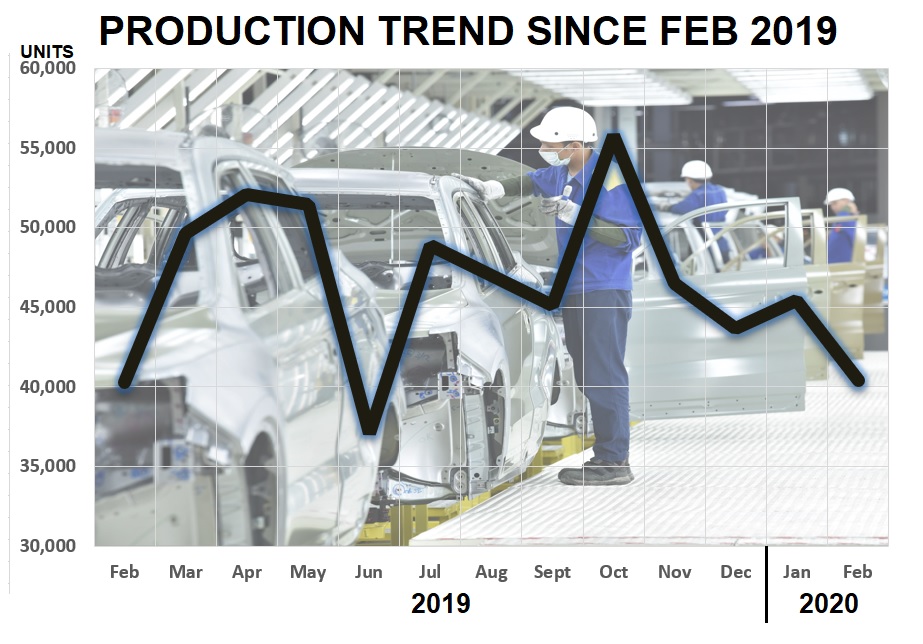

♦ Production of new vehicles dipped 11.1% after the upswing in January. As demand could be seen to be slowing down, many companies would have cut output to avoid building up too many stocks.

♦ The total output of 40,371 units during February 2020 was 17% lower than that of the same month in 2019.

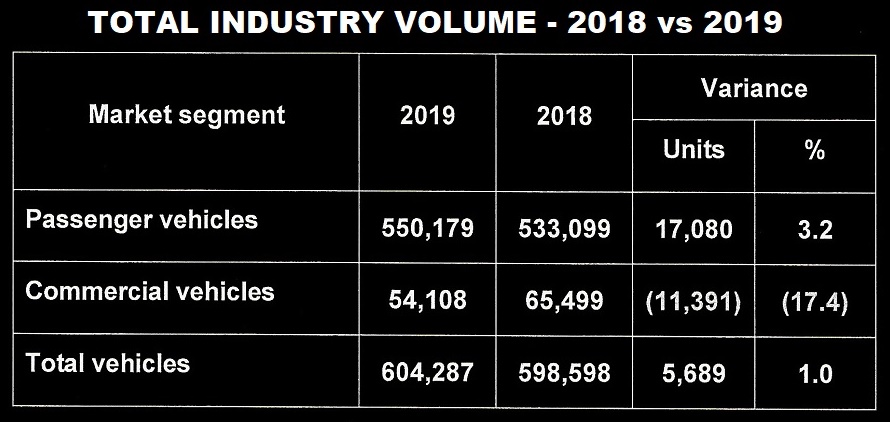

♦ The Total Industry Volume (TIV) in 2019 was 604,287 units, the first time that the volume of sales crossed the 600,000 level since 2015. The achievement was helped by a boost in December with total sales of 54,842 units, the second highest monthly volume in 2019.

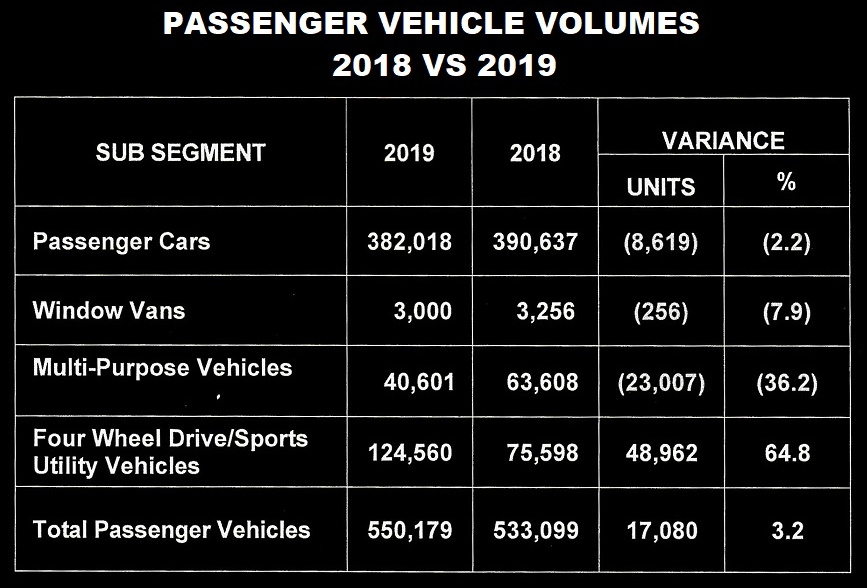

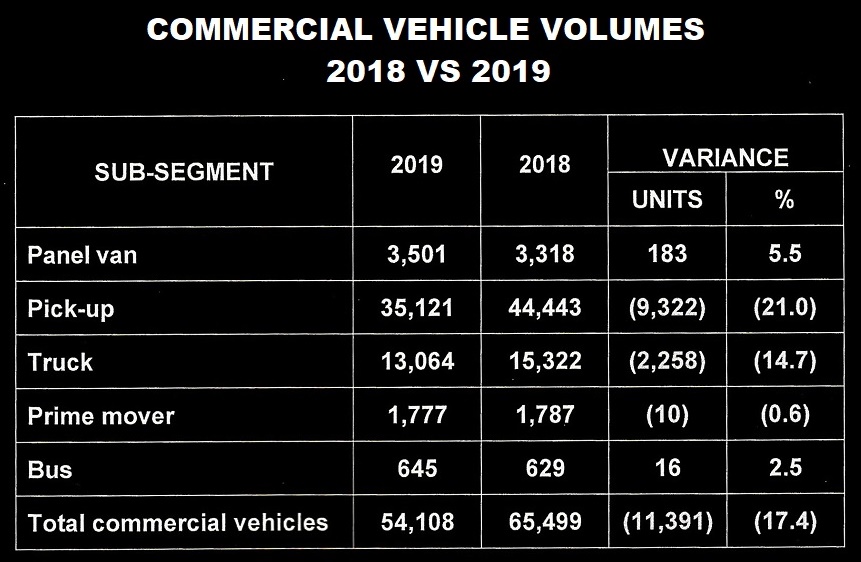

♦ While sales of passenger vehicles rose by 3.2% compared to the year before, the opposite was the case for the commercial vehicle segment (which includes pick-up trucks) as it saw a decline of 17.4%. The uncertainty of the fate of major projects in the first half of the year as well as a general slowdown of the economy had companies holding back on capital expenditures.

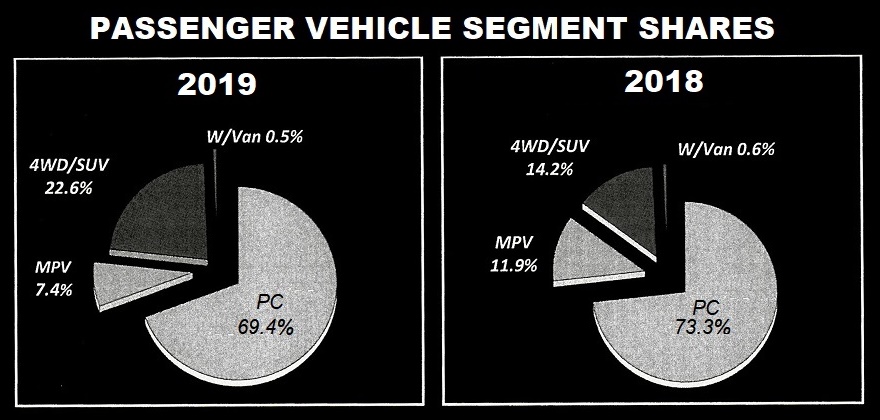

♦ Sales of 4WDs and SUVs grew noticeably (8.4%) at the expense of passenger car and MPV segments, the former contracting by 3.9% and the latter by 4.5%. Nevertheless, passenger cars (sedans and hatchbacks) still accounted for the largest share of passenger vehicle sales (69.4%), while 4WDs/SUVs had a 22.6% share.

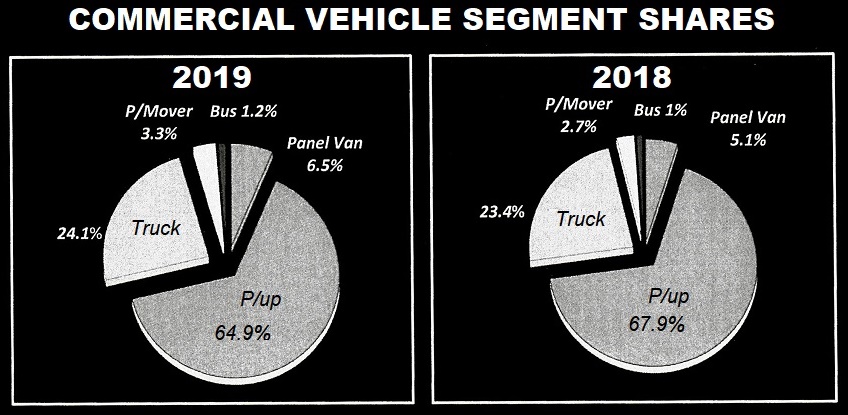

♦ Sales of pick-ups, once a popular segment, fell significantly from 44,443 units in 2018 to 35,121 units in 2019, a reduction of 21%. Nevertheless, these vehicles – which are used for personal transport as well as for business purposes – accounted for almost 65% of commercial vehicle sales.

♦ Local production of vehicles totaled 571,632 units in 2019, a modest 1.2% increase over the output in 2018. While more passenger vehicles were produced (+2.6%), the plants cut back on production of commercial vehicles by 15.6% in the light of uncertain demand.

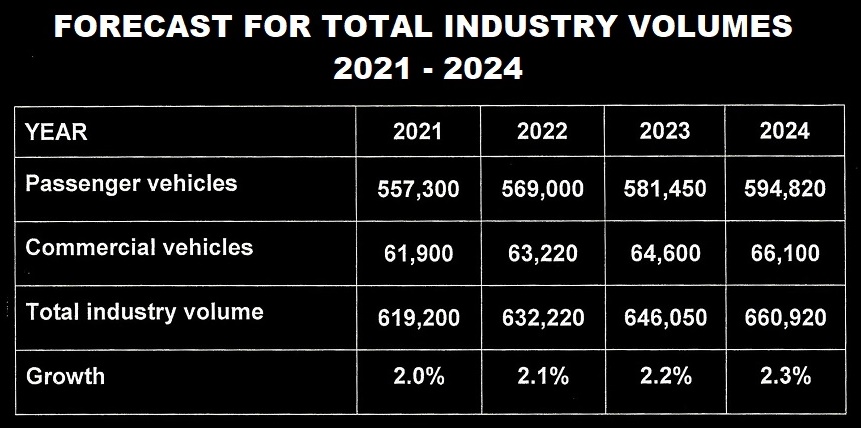

From 2020 to 2024

♦ Looking ahead, the Malaysian Automotive Association (MAA) does not expect the market to grow substantially in 2020 and has forecast a TIV of 607,000 units, just 0.5% more than the 2019 figure. As in the past, this will be reviewed after the first 6 months of sales.

♦ Looking further ahead for the period from 2021 to 2024, the MAA sees the market improving a bit and forecasts annual TIV growth of 2% to 2.3%, reaching 660,920 units by the end of 2024. With sales in Indonesia and Thailand currently around 300,000 units greater, Malaysia will remain at No.3 position in ASEAN.

In the past couple of weeks, there has been speculation that a new tax structure will result in new vehicle prices increasing after the Chinese New Year period. The matter (which related to excise duties) was even documented in the Government Gazette at the end of last year, catching the car companies by surprise.

Needless to say, the public was not happy, especially when it concerned increases in car prices. It’s a sensitive issue because the view is that our car prices are too high and that’s of course due to the taxes imposed. Rather than look at higher sales generating more taxes, the government prefers to just impose heavy taxes to get its revenue which is around RM7 billion a year from the auto industry.

Anyway, you can breathe easy now as the Finance Ministry has confirmed that there will be no increase in new vehicle prices, for the whole of 2020 at least. The good news was conveyed by Datuk Aishah Ahmad, President of the Malaysian Automotive Association (MAA), during the association’s annual press conference to review the market in 2019.

Good news for car companies and consumers

Datuk Aishah said she had actually been informed of a meeting to get the news but she said she was already committed to the press conference so the ministry officials thought it would be a timely announcement she could make when the media was gathered. It was a piece of good news for the industry – something rare as, more often than not, there are new policies which increase the challenges. This time, many people will be able to go off for their holidays relieved that they won’t be coming back to a more difficult situation.

“The Finance Ministry informed me this morning that there will be no increase in the on-the-road price of vehicles due to the transparent reporting of the Open Market Value (OMV). If there is any vehicle affected by this reporting, there will be 100% exemption on the increase incurred until December 31, 2020,” she said.

She was made to understand that any increase in prices as a result of the transparent methodology would be fully absorbed/exempted by the Finance Ministry during 2020, and the difference in duties for past years would also be exempted.

“This is effective immediately and our member companies have been asked to submit the OMV based on the transparent calculation to the Customs Department for those vehicles which are affected by applying the methodology,” Datuk Aishah said.

She explained that the methodology was not actually new and had been applied for years. However, with the transparent calculation, there should be no more disputes over the OMV and this will speed up things. It is understood that the actions of the ministry are related to its obligations as a member of the World Trade Organization (WTO).

Prices of CBU imported vehicles could change from the second half of this year with ‘real-time’ valuations for computing duties.

After 2020?

And what happens in 2021? “Well, we have been informed that there will be further consultations by the industry players with the Finance Ministry and Customs during the year,” she said, adding that the prices of CBU (completely built-up) imports would likely change after May 31, 2020. This is due to a revised method of computation which will be more ‘real-time’ with respect to the value of the vehicles.

So if you were worried that you might have to pay more if you buy after Chinese New Year, that’s not going to be the case. The announcement does not mean that prices won’t change as there are other factors that influence pricing, eg exchange rates, production costs, etc but those are beyond the control of the industry and the government. But as has also been the case for years, the companies will try their best to absorb increases for as long as they can so that their prices remain attractive and competitive.

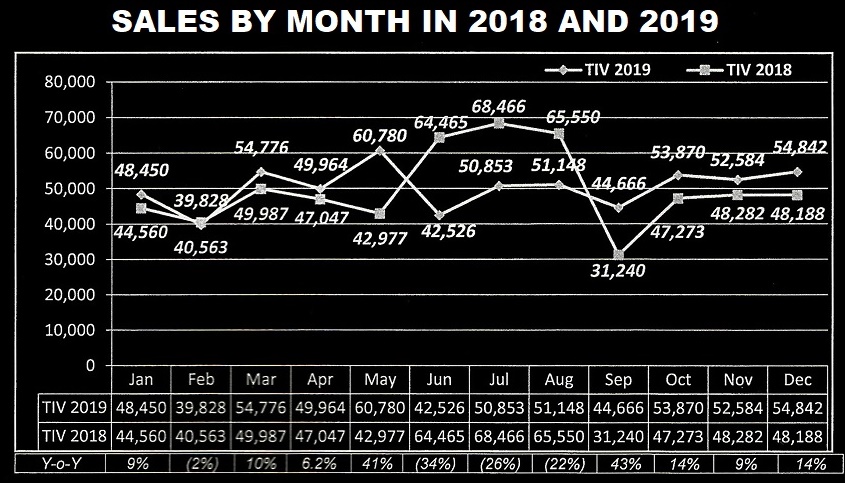

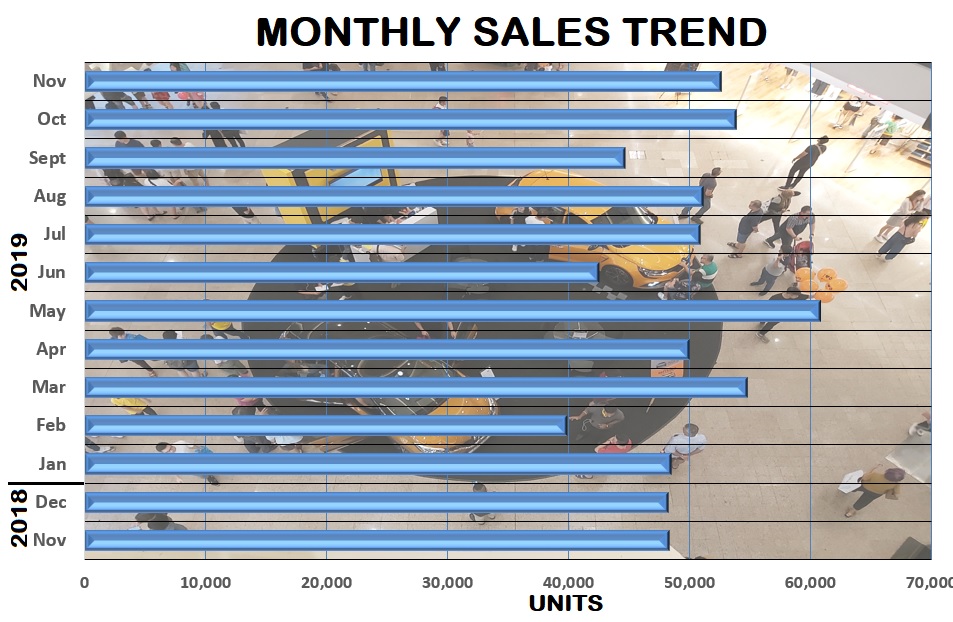

New vehicle sales in the month of November declined by 2.4% or 1,286 units, bringing the Total Industry Volume for the month to 52,584 units of passenger and commercial vehicles. By segment, passenger vehicles accounted for 47,754 units (91%) of the month’s TIV with the remainder being commercial vehicles (including pick-up trucks).

Compared to the same month in 2018 when the market was still in a state of ‘fatigue’ after the surge during the 3 months of GST-free sales, it was to be expected that the figures in 2019 would be higher, with 4,302 units more sold in 2019. A larger volume of passenger vehicles (10% compared to 2018) was sold but commercial vehicles were actually 2% lower.

Source: Monthly reports of the Malaysian Automotive Association (MAA)

As for the TIV for the year to date, ie 11 months, the cumulative volume has reached almost the same level. From January to November, the TIV was 549,445 units which was just 965 units less than for the same period in 2018.

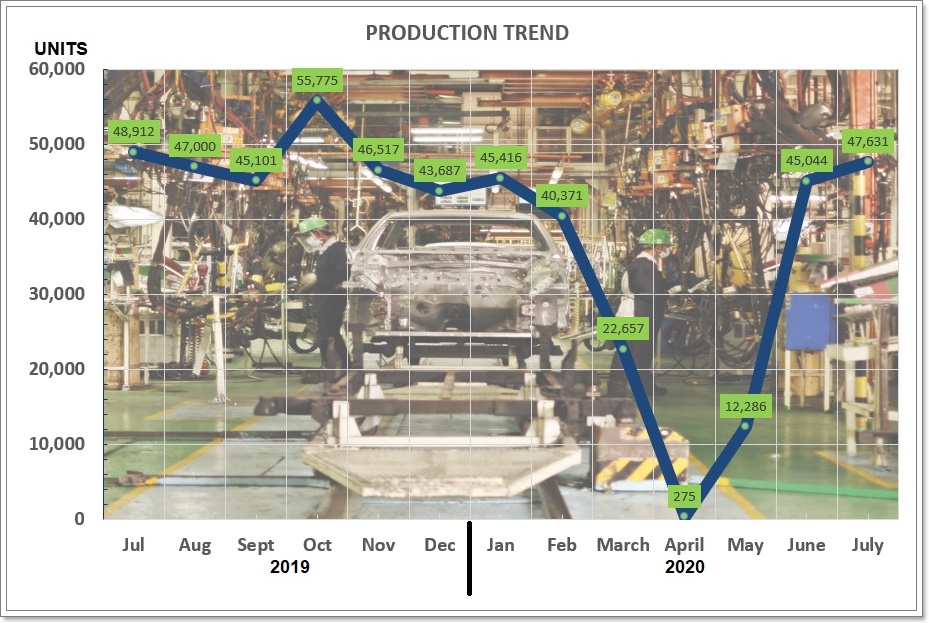

The output of locally-produced vehicles was lower than in November 2018, probably as companies started preparing to scale down stocks with the year coming to an end. 46,517 vehicles were produced, about 8% less than in 2018.

However, the cumulative TIV for 11 months shows that 2019 saw a higher output of 528,333 units where in 2018, the output during the same period was 522,572 units. Passenger vehicles accounted for the boost in numbers but commercial vehicles declined.

A last push to get more sales before 2019 ends.

One month remains and in order to achieve the forecast of 600,000 units for the year by the MAA, 50,555 units would have to be registered in December. This is likely to be possible, with some extra added, as companies will be pushing hard to clear stocks and offer special deals in sales promotions. Many will also be closing their financial year and will want to be able to report the highest numbers to shareholders.

New vehicle sales for October – the first month of the final quarter of 2019 – began on a high note with a 21% increase over the Total Industry Volume (TIV) in September to 53,870 units. This volume was also 14% higher than for the same month in 2018 although a comparison may not be right since it was after the GST-free period when sales had seen a huge boost and the market slowed down in the first few months after that.

The Malaysian Automotive Association (MAA) attributed the increased TIV to more selling days as well as more working days. When there are many holidays, there is also disruption in processes such as registration and loan approvals, delaying completion and affecting deliveries.

Source: Monthly reports of Malaysian Automotive Association

By segment, passenger vehicles (excluding pick-up trucks for personal use) accounted for 93% of the TIV in October, a 16% increase over the same month in 2018. However, commercial vehicle sales were virtually unchanged with 4,883 units (including pick-up trucks) delivered.

The cumulative TIV after 10 months of this year reached 496,861 units which was 5,267 units lower than for the same period in 2018. The higher TIV last year was due to the 3-month GST-free period which saw an above-average surge in monthly sales as buyers could enjoy significant savings (especially for the more expensive models).

Production

The assembly plants collectively produced 55,775 vehicles in October, compared to 51,789 vehicles in the same month in 2018. The increase was largely in the passenger vehicle segment while the commercial vehicle segment declined.

Cumulative production for 10 months was 481,816 units which was 97% of the cumulative sales volume but this direct comparison may not be entirely accurate as there would be an overlap in stocks and imports. Popular models may leave the plants within days of being completed but there may also be vehicles which don’t move out so fast (although the plants would not want them around too long either as they take up parking space).

With two months left to the year and a forecast of 600,000 units for the year by the MAA, it means that sales in November and December must average 51,569 units. This year, 5 months have seen the TIV above 50,000 units and it’s often the case that there is such a big boost in December that the forecast is met.